Working After Retirement

Wondering what happens if you work after retirement? You’re not alone. Working after retirement has its benefits if you're missing a sense of purpose. If returning to work, be mindful that the IRS imposes certain limits and rules that can impact your Social Security benefits, Medicare coverage, pensions and other retirement accounts.

- Written by Terry Turner

Terry Turner

Senior Financial Writer and Financial Wellness Facilitator

Terry Turner has more than 35 years of journalism experience, including covering benefits, spending and congressional action on federal programs such as Social Security and Medicare. He is a Certified Financial Wellness Facilitator through the National Wellness Institute and the Foundation for Financial Wellness and a member of the Association for Financial Counseling & Planning Education (AFCPE®).

Read More- Edited By

Lamia Chowdhury

Lamia Chowdhury

Financial Editor

Lamia Chowdhury is a financial content editor for RetireGuide and has over three years of marketing experience in the finance industry. She has written copy for both digital and print pieces ranging from blogs, radio scripts and search ads to billboards, brochures, mailers and more.

Read More- Published: November 30, 2020

- Updated: October 20, 2023

- 22 min read time

- This page features 35 Cited Research Articles

- Edited By

- Working after retirement can impact your Social Security benefits, Medicare and health insurance coverage, pensions and retirement accounts.

- Social Security benefits get complicated if you return to work and start making money. The Social Security Administration uses a term called “combined income” to determine how much of your check can be taxed. Combined income is a combination of your adjusted gross income and nontaxable interest plus half of your yearly Social Security benefit.

- You can take private health insurance and still keep your Medicare coverage if you return to work for an employer who offers it. Medicare can be either your primary or secondary coverage.

- Returning to work after retiring may affect your pension due to certain tax rules and conditions. If you go back to work, consider adding money to your retirement accounts.

Retirement was once a destination — a goal post to mark the end of a long, productive career.

But research indicates that retirement is becoming much more fluid in America.

A 2017 survey from RAND Corporation, a nonprofit research firm, found that almost 40% of workers over age 65 had previously retired — only to rejoin the workforce.

And for those still in retirement, roughly half said they would return to paid work if the right opportunity presented itself.

According to researchers: “The fact that these individuals have access to Social Security benefits and possibly other retirement income suggests they can afford to demand working conditions that more closely match their preferences in order to participate in employment.”

So, what motivates people to “unretire” or start an encore career?

“If you’re thinking about returning to work, one of two things has happened,” Accredited Financial Counselor Susan Greenhalgh told RetireGuide. “You’ve either been struck with a severe case of boredom and miss the sense of purpose working gives you — or you’re feeling a financial pressure to go back, maybe due to an emergency.”

What Are the Pros and Cons of Returning to the Workforce?

In late 2021, during the COVID-19 pandemic, more than half of American adults 55 and older had left the workforce, according to an analysis by the Pew Research Center. But many people who retired early may be having second thoughts.

More than 10 million Americans ages 65 and older remain in the labor force, according to the Bureau of Labor Statistics. Another nearly 26 million ages 55 to 65 are also working. And the Census Bureau reports a trend of older Americans remaining in or returning to the workforce.

There are pros and cons to back out of retirement and return to work. You may want to compare them and consider your personal desire to return to work to determine your best options.

What Are the Benefits of Returning to the Workforce?

Returning to work offers benefits ranging from extra income to returning to a career that gave you enjoyment or a sense of purpose.

Some of the benefits may depend on whether you enrolled in Social Security at your full retirement age and whether you are enrolled in Medicare.

*Ad: Clicking will take you to our partner Annuity.org.

Pros of Returning to Work in Retirement

- Extra Income

- Going back to work can add extra income to your bank account. You can also put more money into an employer-sponsored retirement account — and if you’re 50 or older, make larger annual contributions. More income can also add to the amount of monthly Social Security benefits you can draw. Extra income in retirement can make it easier to pay essential bills while stretching your retirement savings.

- Health Insurance

- Group health insurance through your employer can work with Medicare through coordination of benefits. And a group plan through work may end up saving you money if you are on Medicare when you return to work. You may be able to delay Medicare Part B and Part D enrollment while you’re working. This could save you hundreds of dollars a month.

- Easing boredom

- Work can provide mental stimulation. If you enjoyed working and found meaning through your job, then going back to work may help ease boredom. You could even benefit from trying a new career path to learn new things.

- Social connections

- It becomes difficult to create new social connections in retirement. Jobs provide structure and put you into close contact with coworkers. Going back to work can give you almost instant social connections.

Risks of Returning to the Workforce

You should also consider the downsides of returning to the workforce. While some downsides may be the obstacles that come with rejoining the workforce, others may be financial losses you could suffer.

Cons of Returning to Work in Retirement

- Ageism in the workplace

- Nearly 80% of older workers returning to the workforce following the COVID-19 pandemic reported confronting ageism, according to a survey by AARP. Workers reported that they were asked to provide birth and graduation dates, as well as other age-related information, on job applications or in job interviews. Older workers were displaced twice as long as younger individuals, and many report earning less than their previous job.

- Less free time

- Your time is no longer your own if you return to work. One of the most appealing aspects of retirement is the ability to set your own hours. That disappears when you have to punch a time clock again. Your schedule may become even more random if you decide on a part-time job.

- Reduced Social Security benefits

- Working after retirement can put a dent in your Social Security benefits. If you retired and enrolled in Social Security when you turned 62, then you could see your benefits reduced by as much as 30% until you reach your full retirement age. Social Security deducts one dollar from every two dollars you earn above a fixed amount. The Social Security Administration updates the threshold for benefits while working each year.

- Risk of higher taxes

- The extra income from returning to work could bump you into a higher tax bracket — meaning, you have to pay higher income taxes. If your combined income hits certain thresholds, then up to 85% of your Social Security benefits could be taxable. You’ll also have to pay state and local income taxes — depending on where you live and work — on your new income.

Financial Considerations of Working After Retirement

Returning to work is a unique, personal decision.

But before you head back, experts like Greenhalgh say it’s essential to get a firm grasp on your current cash flow and budget.

“You need your eyes wide open to your own financial situation,” said Greenhalgh, who started her business, Mind Your Money LLC, in 2018 at the age of 62. “You need to be honest with yourself about your needs and your capabilities.”

Working in retirement can supplement your income but it’s important to understand what you’ll be gaining — and potentially losing — in the process.

- Social Security benefits.

- Medicare and health insurance coverage.

- Pensions.

- Retirement accounts.

“It’s important to do a deep dive into these things first,” Greenhalgh said. “Otherwise, you’re going to be surprised at how your benefits may be impacted.”

“You need your eyes wide open to your own financial situation.”

If money is your primary motivator, look for jobs with wages and benefits that fill your income gaps without jeopardizing your benefits or negatively affecting your bottom line.

*Ad: Clicking will take you to our partner Annuity.org.

How Working Affects Your Social Security Benefits

You can return to work and still collect Social Security retirement benefits.

But certain limits and rules must be followed.

Adrienne Ross is a financial planner in Spokane, Washington. She told RetireGuide that many people take Social Security benefits at age 62 — even if they have money saved in a retirement account.

“It often seems like a safe, secure idea to take those benefits as soon as possible,” said Ross, founder of Clear Insight Financial Planning.

But starting Social Security when you’re first eligible reduces your benefits by as much as 25% to 30%.

“People may claim Social Security at 62 only to go back to work a few years later because they’re not getting as much money in benefits as they anticipated,” Ross explained.

Your age determines how much you can earn.

| Year of Birth | Full Retirement Age |

|---|---|

| 1955 | 66 years and 2 months |

| 1956 | 66 years and 4 months |

| 1957 | 66 years and 6 months |

| 1958 | 66 years and 8 months |

| 1959 | 66 years and 10 month |

| 1960 and later | 67 |

In 2022, you can earn up to $19,560 without impacting your benefits before full retirement age.

However, once you hit that threshold, your Social Security check goes down $1 for every $2 earned.

For example, you start collecting Social Security benefits at age 62. At age 64, you get a part-time job and earn $25,000 in a year.

This is $5,440 over the limit. Your Social Security check will be reduced by $2,720 that year — or $1 for every $2 earned.

In the year you reach your full retirement age, you can earn up to $51,960 in 2022 before your benefits are docked. After the $51,960 threshold, your benefits are reduced by $1 for every $3 earned.

Finally, once you hit your full retirement age, there is no cap to your income and you can even increase your Social Security benefits if you choose to continue working. Should your benefits increase, the Social Security Administration will send you a letter informing you of your new benefit amount.

You will still continue to pay Social Security taxes on your earnings for each additional year you work.

Social Security Benefits and Taxes

If Social Security is your only source of income, you don’t need to worry about paying taxes on your benefits.

But things get more complicated if you return to work and start making money.

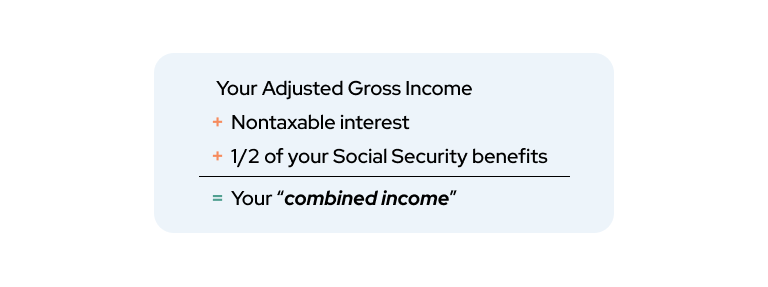

The Social Security Administration uses a term called “combined income” to determine how much of your check can be taxed.

- Adjusted gross income (This is the amount you get paid at work — before taxes are taken out — minus adjustments, such as contributions to certain retirement accounts, HSAs and other applicable deductions).

- Nontaxable interest.

- One-half of your yearly Social Security benefit.

If that combined income number is less than $25,000 for an individual, then your Social Security benefits aren’t taxable.

If your combined income is between $25,000 and $34,000 for a single filer, you may owe income tax on up to 50% of your benefits.

If your combined income is more than $34,000, up to 85% of your benefits can be taxed.

Each January, you’ll receive a Social Security Benefit Statement, Form SSA-1099. Use this when you complete your federal return to see if you owe taxes on your benefits.

Social Security benefit taxation is complicated. Reach out to a tax professional or financial planner if you need help.

Other Social Security Considerations

It’s smarter financially to delay Social Security benefits until your full retirement age, Ross said.

Still, there’s a couple ways to recoup at least some of those losses.

First, if your benefits were reduced because you made more than the income limits mentioned earlier, you actually get that money back — eventually. It isn’t gone forever.

Here’s how it works.

Let’s assume you take Social Security at age 62 and receive a monthly benefit of $1,000. At age 63, you decide to go back to work.

You work for 12 months and earn more than the $19,560 income limit. Your Social Security benefits are reduced to $500 for 12 months as a result.

Once you hit full retirement age, those 12 months of reduced benefits are paid back to you.

In this case, you’d receive your normal $1,000 monthly benefit plus $500 for 12 months.

After that, your benefit goes back to your standard $1,000 a month.

Here’s something else to keep in mind: Your Social Security check is based on your top 35 years of earnings.

If your latest year of work turns out to be one of your highest, Social Security will refigure your monthly benefit and you may see a boost in your check once you hit your full retirement age.

This is different than recouping your reduced benefits, and it likely won’t affect you if you returned to work for a low-paying or part-time job.

For more information about working and Social Security benefits, check out the SSA’s How Work Affects Your Benefits booklet.

Medicare, Private Insurance and Post-Retirement Work

If you’re 65 or older, you likely get health insurance from Medicare or a Medicare Advantage plan.

Original Medicare is made up of two parts — Part A hospital insurance and Part B medical coverage. You may also choose to purchase a standalone Medicare Part D prescription drug plan or a Medigap supplement insurance policy.

Most people don’t pay a monthly premium for Medicare Part A. But nearly everyone pays a monthly premium for Medicare Part B. In 2024, the Part B premium is $174.70.

If you return to work for an employer who offers private health insurance, you can take it and still keep your Medicare coverage. You’re allowed to have both.

Medicare may act as your primary coverage or your secondary coverage.

You may consider dropping Medicare Part B if you return to work. Some people do this to avoid paying the $174.70 monthly premium in addition to any employer health care costs.

However, this can be tricky. If you’re not careful, you may owe penalties and face other issues down the road.

First, your employer must have more than 20 employees. If that’s not the case, you may be penalized for dropping Medicare Part B.

If you have active employer coverage, you can choose to disenroll from Medicare Part B.

Once you lose your employer health insurance or return to retirement, you must sign up for Part B again within eight months.

Otherwise, you may face a lifetime late enrollment penalty.

Meanwhile, you only get two months to sign up for a standalone Part D plan once your workplace coverage ends. You can face a late-enrollment penalty for this, too.

To disenroll from Medicare, you’ll need to submit a form, CMS-1763, and it must be completed during an interview with a Social Security representative.

Medicare Coverage for High-Income Earners

Let’s say you return to work after age 65 and keep your Medicare coverage.

If you land a lucrative second career or consulting position, you may enter a higher income bracket and face Medicare surcharges.

That’s because, by law, high-income earners pay more for Medicare Part B and Part D.

If you’re single and earn more than $103,000 but less than or equal to $129,000 a year, you must pay an additional $69.90 a month for your Part B premium in 2024.

For a married couple filing jointly, extra charges start at incomes above $206,000.

A similar, smaller surcharge applies to Part D premiums.

In 2024, an individual who makes between $97,000 and $129,000 a year will owe a $12.90 income-related monthly adjustment amount in addition to their standard Part D premium.

Pensions and Retirement Accounts

Pensions and retirement accounts are two additional ways people supplement income in later life.

But certain tax rules and conditions need to be considered if you’re rejoining the workforce.

How Returning to Work Can Impact Pensions

Returning to work after retiring may affect your pension.

Each pension is different, so it’s important to look at your plan’s details.

Sometimes, you must be rehired as a part-time or contract worker if you want to work for your former employer and still receive pension benefits.

Other times, returning to work for a former employer will suspend your pension benefits.

You can usually still collect a pension and work full-time so long as it’s with a different company.

Check with your human resources department and your pension plan provider first to understand any potential penalties.

Retirement Accounts and Required Minimum Distributions

Certain retirement accounts, including 401(k)s and IRAs, follow a tax rule called required minimum distribution, or RMD.

This requires retirement plan account owners to withdraw money starting at age 72, or 73 if you turn 72 after Dec. 31, 2022.

Even if you continue working past 72, you must take a RMD from your IRA.

If you don’t, you’ll face a potential 25% tax penalty.

You might be able to delay taking RMDs from your current employer-sponsored retirement account, such as a 401(k), 457(b), or 403(b).

- Still be working.

- Have an employer-sponsored retirement account with the business you work for.

- Own less than 5% of the company you work for.

If you go back to work, consider adding money to your retirement accounts.

A law known as the SECURE Act of 2019 makes this possible. It allows all retirees to contribute to traditional IRAs and 401(k)s if they earn wages.

People over age 50 can contribute up to $7,500 a year to an IRA in 2023. And if your company offers a 401(k) match, take it. It’s essentially free money.

“This can help increase your savings if you maybe didn’t have much money in savings before returning to work,” Ross told RetireGuide.

Contributing to a retirement account can also help offset taxes owed on your Social Security benefits because adding money to an IRA or 401(k) plan shrinks your adjusted gross income, Ross added.

How Do You Find a Job in Retirement?

Understand that it becomes more difficult to find a job after you turn 50 — whether you retired from your last gig or not.

Returning to the workforce after retirement can bring an extra set of difficulties. Be prepared to face bias but keep an optimistic attitude. All job seekers must deal with rejection before landing the job they want. That may be even more so if you’re returning from retirement.

You’ll also need to identify the type of job you want and why you want it — part time, full time, a return to your old career or starting something entirely new to you.

Steps to Launch Your Job Search After Retirement

Network online

Create a professional online presence. Update or launch work-specific accounts on LinkedIn, Facebook, Instagram and Twitter. Post and comment on elements of your profession or career. These can help showcase your career expertise. Use your social media connections to connect with potential employers and find job opportunities.

Create an age-proof resume

Highlight your experience without referencing your age. Keep your resume short, including only relevant or recent jobs — but highlighting your accomplishments under a “Career Highlights” section at the top. Get rid of graduation dates or any other references that may give away your age. Make sure your email address is updated and timely and list your cell phone number — never your landline. Don’t include a fax number. Include social media info — particularly related to the professional profile you’ve created with career-related social media accounts.

Online job search focused on older workers

There are online job search sites that specialize in connecting retirees and older workers with companies looking to hire, as well as sites that provide resources for older workers looking to get back into the workforce.

- FlexJobs.com: This site specializes in flexible, part-time, freelance and remote-working positions.

- Retired Brains: In addition to helping you launch your own business, this site also lists seasonal, online and remote jobs for retirees.

- RetirementJobs.com: This site matches older workers to companies most likely to hire experienced employees.

- Seniors4Hire: This site bills itself as an online community for employers recruiting workers ages 50 and older that lets you post a resume and search job openings.

- WorkForce50.com: This site focuses on jobs for workers 50 and older, letting you search by location or by employer.

Job Fairs

Traditional job search avenues may still be helpful. A job fair can force you to network and do other aspects of your job search that are vital — but that most people tend to dislike. It also gives you a chance to meet company representatives face-to-face, making you more than just another resume or application. Plus, it gives you immediate feedback on your resume and experience and how an employer reacts to them.

Self-Employment

Retirement is an ideal time to try your hand at self-employment — especially if you have retirement savings to support yourself. If there’s a hobby you want to turn into a business or a line of work you always wanted to try, this may be a route back to the workforce.

What Environment Should You Work In?

You should carefully consider the type of work environment you want to be a part of before starting your workforce job hunt. The COVID-19 pandemic and subsequent “Great Resignation” has significantly changed where, when and how Americans work.

There are different advantages and disadvantages that make different work environments ideal for different people.

- In-person or on-site

- You may want to consider an on-site job if your desire to return to the workplace is heavily driven by a desire for social connections. It may also be better for you if you are looking for the structure you miss from working on-site during your career.

- Remote work

- Remote work means no commutes and the ability to work for an employer across the country without having to pack up and move. If you enjoy working on your own — from anywhere — you may want to consider jobs that offer this option.

- Flexible workplaces

- Flexible workplaces bring together the best of both worlds. They allow you to work on-site with co-workers sometimes while working remotely at other times. Hybrid environments can give you social interaction with the flexibility to work from home or on the road. It may also mean working either part-time or full-time, which gives you flexibility in how much of your retirement time you want to give up to an employer.

Remote working has also created new job opportunities for people with limited mobility or other conditions that may make a traditional workplace less appealing.

*Ad: Clicking will take you to our partner Annuity.org.

Ask an Expert: Tips for Working After Retirement

Liz Lopez founded her company, Captivate Your Audience Business Services, 13 years ago in Tampa Bay, Florida. She provides resume design, job search strategies, LinkedIn training and other services to clients who want to stand out in a competitive, 21st century job market.

Think about what you want to do. What brings you joy in the workplace? Too often professionals make themselves miserable because they go after what they think is available rather than what makes them happy.

Late career is a lousy time to be stuck in a job you don’t enjoy. Figure out what feels rewarding, then do the research to determine what jobs or businesses align with your goals and skills.

Embrace how things work now. The job market changes constantly. There is more automation, it’s a lot less personal and it can move very slowly. By marketing yourself strategically, you can land an opportunity where you make a meaningful impact and leave a valuable legacy.

MORE: Roth IRA for Kids: How To Make Your Grandchildren Millionaires

Be prepared to develop a resume, cover letter and LinkedIn profile that aligns with current job market trends. Then learn how to interview effectively via video. You need to powerfully show that you are relevant in today’s world.

Focus on your history and achievements from the last 10 to 15 years. Otherwise, you can age yourself out of consideration if you insist on talking about work you did 30 years ago. Ageism is sadly very real.

If you are not sure how to get started, find a career coach experienced with mature and late-career professionals. Whichever route you take, consult with your accountant or tax professional to understand the impact of any new income.

Additional Resources

- CareerOneStop

- CareerOneStop is a comprehensive career, training and job search website sponsored by the U.S. Department of Labor. It offers many free online tools, including a job board, articles, training resources and more. You can also find local help by entering your city or zip code into the American Job Center finder on the website.

- Goodwill Industries

- Local Goodwill employment specialists can provide a blend of in-person and virtual services, classes and training programs in various fields. They also offer resume assistance and virtual job fairs. Call 1-800-466-3945 or visit goodwill.org to search for your local Goodwill by zip code.

- Senior Community Service Employment Program

- The Senior Community Service Employment Program connects low-income, unemployed adults age 55 and older with community service work at nonprofit and public facilities, such as schools, hospitals and senior centers. Participants work an average of 20 hours a week at minimum wage and are provided free training as a bridge to unsubsidized employment. For more information, call 1-877-872-5627, or visit the online Older Worker Program Finder.

"This was great. Cleared up a lot of my questions. Straight talk I could understand. Thank you!"

Connect With a Financial Advisor Instantly

Our free tool can help you find an advisor who serves your needs. Get matched with a financial advisor who fits your unique criteria. Once you’ve been matched, consult for free with no obligation.

- Association for Financial Counseling & Planning Education (AFCPE®) member

- Holds six Health Literacy certificates from the CDC

- Emmy® Award winner

35 Cited Research Articles

- U.S. Centers for Medicare & Medicaid Services. (2023, October 12). 2024 Medicare Parts A & B Premiums and Deductibles. Retrieved from https://www.cms.gov/newsroom/fact-sheets/2024-medicare-parts-b-premiums-and-deductibles

- U.S. Centers for Medicare & Medicaid Services. (2022, September 27). 2023 Medicare Parts A & B Premiums and Deductibles 2023 Medicare Part D Income-Related Monthly Adjustment Amounts. Retrieved from https://www.cms.gov/newsroom/fact-sheets/2023-medicare-parts-b-premiums-and-deductibles-2023-medicare-part-d-income-related-monthly

- Eisenberg, R. (2022, May 21). “I Needed Something to Do”: How Working In Retirement Is Being Embraced by Older Adults and Companies. Retrieved from https://www.marketwatch.com/story/i-needed-something-to-do-how-working-in-retirement-is-being-embraced-by-older-adults-and-companies-11652788447

- Casselman, B. (2022, May 19). “I Had to Go Back”: Over 55, and Not Retired at All. Retrieved from https://www.nytimes.com/2022/05/19/business/economy/older-workers-labor-force.html

- Bhattarai, A. (2022, May 6). Millions Retired Early During the Pandemic. Many Are Now Returning to Work, New Data Shows. Retrieved from https://www.washingtonpost.com/business/2022/05/05/retirement-jobs-work-inflation-medicare/

- Nova, A. (2022, March 20). How Older Workers Can Push Back Against the Reality of Ageism. Retrieved from https://www.cnbc.com/2022/03/20/how-older-workers-can-push-back-against-the-reality-of-ageism-.html

- U.S. Bureau of Labor Statistics. (2022, January 20). Labor Force Statistics from the Current Population Survey. Retrieved from https://www.bls.gov/cps/cpsaat18b.htm

- Social Security Administration. (2022). How Work Affects Your Benefits. Retrieved from https://www.ssa.gov/pubs/EN-05-10069.pdf

- Fry, R. (2021, November 4). Amid the Pandemic, a Rising Share of Older U.S. Adults Are Now Retired. Retrieved from https://www.pewresearch.org/fact-tank/2021/11/04/amid-the-pandemic-a-rising-share-of-older-u-s-adults-are-now-retired/

- Social Security Administration. (n.d.). Retirement Benefits. Retrieved from https://www.ssa.gov/benefits/retirement/planner/whileworking.html

- Centers for Medicare & Medicaid Services. (2020, November 6). 2021 Medicare Parts A & B Premiums and Deductibles. Retrieved from https://www.cms.gov/newsroom/fact-sheets/2021-medicare-parts-b-premiums-and-deductibles

- HBS Working Knowledge. (2020, October 15). How Much Will Remote Work Continue After The Pandemic? Retrieved from https://www.forbes.com/sites/hbsworkingknowledge/2020/10/15/how-much-will-remote-work-continue-after-the-pandemic/?sh=17b3bc8510a9

- Jacobson, G., Feder, J. and Radley, D. (2020, October 6). COVID-19’s Impact on Older Workers: Employment, Income, and Medicare Spending. Retrieved from https://www.commonwealthfund.org/publications/issue-briefs/2020/oct/covid-19-impact-older-workers-employment-income-medicare

- Internal Revenue Service. (2020, September 23). Retirement Topics — Required Minimum Distributions (RMDs). Retrieved from https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-required-minimum-distributions-rmds

- Internal Revenue Service. (2020, September 19). Retirement Plan and IRA Required Minimum Distributions FAQs. Retrieved from https://www.irs.gov/retirement-plans/retirement-plans-faqs-regarding-required-minimum-distributions#1

- Bartik, A., Cullen, Z., Glaeser, E., et al. (2020, July 29). What Jobs Are Being Done at Home During the COVID-19 Crisis? Evidence from Firm-Level Surveys. Retrieved from https://hbswk.hbs.edu/item/what-jobs-are-being-done-at-home-during-the-covid-19-crisis-evidence-from-firm-level-surveys

- Rapacon, S. (2020, June 18). How Older Adults Can Find Work-at-Home Jobs During the Pandemic. Retrieved from https://www.aarp.org/work/job-search/finding-work-from-home-jobs/

- Internal Revenue Service. (2020, February 18). Publication 969 2019 Health Savings Accounts and Other Tax-Favored Health Plans. Retrieved from https://www.irs.gov/publications/p969#en_US_2019_publink1000204138

- Social Security Administration. (2020). Fact Sheet: 2021 Changes to Social Security. Retrieved from https://www.ssa.gov/news/press/factsheets/colafacts2021.pdf

- Social Security Administration. (2020). How Work Affects Your Benefits. Retrieved from https://www.ssa.gov/pubs/EN-05-10069.pdf

- Social Security Administration. (2020). Retirement Benefits. Retrieved from https://www.ssa.gov/pubs/EN-05-10035.pdf

- O’Brien, S. (2019, August 12). Dropping Medicare for employer health coverage may trip you up. Retrieved from https://www.cnbc.com/2019/08/12/dropping-medicare-for-employer-health-coverage-may-trip-you-up.html

- United Income. (2019, April 27). Older Americans in the Workforce. Retrieved from https://unitedincome.capitalone.com/library/older-americans-in-the-workforce

- Edleson, H. (2019, April 22). More Americans Working Past 65. Retrieved from https://www.aarp.org/work/employers/americans-working-past-65/

- Edleson, H. (2018, September 12). Working After Retirement: Beware the Cost. Retrieved from https://www.aarp.org/retirement/planning-for-retirement/info-2018/going-back-to-work-ss.html

- O’Brien, S. (2018, August 13). How part-time work in retirement can affect Social Security taxes and Medicare costs. Retrieved from https://www.cnbc.com/2018/08/13/part-time-work-in-retirement-can-affect-social-security-and-medicare.html

- Span, P. (2018, March 30). Many Americans Try Retirement, Then Change Their Minds. Retrieved from https://www.nytimes.com/2018/03/30/health/unretirement-work-seniors.html

- Maestas, N., Mullen, K., Powell, D., et al. (2017). Working Conditions in the United States: Results of the 2015 American Working Conditions Survey. Retrieved from https://www.rand.org/pubs/research_reports/RR2014.html

- Barry, P. (2014, April). Disenrolling from Part B. Retrieved from https://www.aarp.org/health/medicare-insurance/info-05-2008/ask_ms__medicare_5.html

- CareerOneStop.org. (n.d.). Older worker. Retrieved from https://www.careeronestop.org/ResourcesFor/55PlusWorkers/55-plus-workers.aspx?lang=en&frd=true

- Centers for Medicare & Medicaid Services. (n.d.). Medicare Decisions for Those Over 65 and Planning to Retire in the Next Six Months. Retrieved from https://www.cms.gov/Outreach-and-Education/Find-Your-Provider-Type/Employers-and-Unions/FS4-Medicare-for-people-over-65-nearing-retirment.pdf

- Medicare.gov. (n.d.). How Medicare works with other insurance. Retrieved from https://www.medicare.gov/supplements-other-insurance/how-medicare-works-with-other-insurance

- Centers for Medicare & Medicaid Services. (n.d.). 2022 Medicare Parts A & B Premiums and Deductibles/2022 Medicare Part D Income-Related Monthly Adjustment Amounts. Retrieved from https://www.cms.gov/newsroom/fact-sheets/2022-medicare-parts-b-premiums-and-deductibles2022-medicare-part-d-income-related-monthly-adjustment

- Social Security Administration. (n.d.). Benefit Calculators. Retrieved from https://www.ssa.gov/benefits/calculators/

- Social Security Administration. (n.d.). Income Taxes And Your Social Security Benefit. Retrieved from https://www.ssa.gov/benefits/retirement/planner/taxes.html

Calling this number connects you to one of our trusted partners.

If you're interested in help navigating your options, a representative will provide you with a free, no-obligation consultation.

Our partners are committed to excellent customer service. They can match you with a qualified professional for your unique objectives.

We/Our Partners do not offer every plan available in your area. Any information provided is limited to those plans offered in your area. Please contact Medicare.gov or 1-800-MEDICARE to get information on all of your options.

844-359-1705Your web browser is no longer supported by Microsoft. Update your browser for more security, speed and compatibility.

If you need help pricing and building your medicare plan, call us at 844-572-0696