How to Pay Off Debt

The average American household carries nearly $120,000 in debt. Paying it down plays a major role in any successful retirement planning strategy. There are different approaches to eliminating debt, but to be successful, you need to find the best strategy that works for you.

- Written by Terry Turner

Terry Turner

Senior Financial Writer and Financial Wellness Facilitator

Terry Turner has more than 35 years of journalism experience, including covering benefits, spending and congressional action on federal programs such as Social Security and Medicare. He is a Certified Financial Wellness Facilitator through the National Wellness Institute and the Foundation for Financial Wellness and a member of the Association for Financial Counseling & Planning Education (AFCPE®).

Read More- Edited By

Lee Williams

Lee Williams

Senior Financial Editor

Lee Williams is a professional writer, editor and content strategist with 10 years of professional experience working for global and nationally recognized brands. He has contributed to Forbes, The Huffington Post, SUCCESS Magazine, AskMen.com, Electric Literature and The Wall Street Journal. His career also includes ghostwriting for Fortune 500 CEOs and published authors.

Read More- Financially Reviewed By

Ebony J. Howard, CPA

Ebony J. Howard, CPA

Credentialed Tax Expert at Intuit

Ebony J. Howard is a certified public accountant and freelance consultant with a background in accounting, personal finance, and income tax planning and preparation. She specializes in analyzing financial information in the health care, banking and real estate sectors.

Read More- Published: September 1, 2021

- Updated: August 12, 2023

- 10 min read time

- Edited By

Types of Debt

Debt can be a powerful financial tool to improve your life or burdensome baggage that creates a drag on your financial well-being. Understanding how to handle debt, knowing the difference between “good” and “bad” debt, and having a strategy to pay off debt is essential to your financial wellness.

Personal debt in the United States totaled $14.6 trillion in 2021 — nearly $120,000 per household. The bulk of this is made up of mortgage and home equity loans, student loans, auto loans and credit card debt.

| TYPE OF DEBT | TOTAL DEBT IN US (2021) | AVERAGE DEBT PER HOUSEHOLD |

|---|---|---|

| Mortgage (and home equity loans) | $10.0 trillion | $81,300 |

| Student loans | $1.6 trillion | $13,008 |

| Auto loans | $1.4 trillion | $11,382 |

| Credit card debt | $819 billion | $6,659 |

| Other debt | $781 billion | $6,349 |

| Total debt | $14.6 trillion | $118,698 |

Other personal debt in the U.S. includes medical debt, personal loans, business debt and money owed to collection agencies.

Good Debt vs. Bad Debt

Taking on debt is the only way most Americans can afford a home. But trying to pay off debt can drain your resources. That’s why you may hear about “good debt” and “bad debt.”

Good debt – such as buying a house – may improve your life in an important way or increase your net worth. Houses not only provide shelter and a home for your family, they tend to appreciate in value, giving you an investment toward your future net worth.

Bad debt involves loans you take out to cover purchases that quickly depreciate in value or have a high interest rate. Failing to quickly pay off a credit card purchase can sometimes turn into bad debt.

The key to determining whether something is good or bad debt often depends on your financial situation and how much you can afford to pay — and to lose — on the money you borrow.

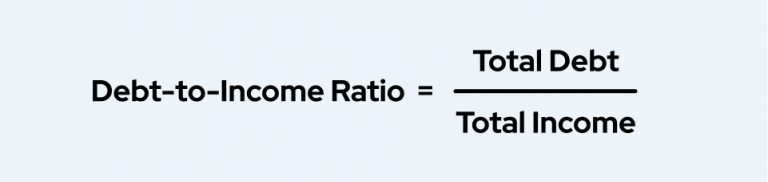

Understanding Debt Ratios

Knowing your debt ratio is a good way to avoid getting too deeply into debt. Your debt ratio is the total value of your debt divided by your after-tax income. You can calculate this two different ways: with and without counting your mortgage.

This formula will tell you what percentage of your income is going toward paying off your debt.

As a rule of thumb, having a debt ratio of 10 to 36 percent is considered manageable — no higher than 10 percent if you don’t include your mortgage, 36 percent if you include it in your calculation.

Amounts higher than those are generally considered unmanageable by lenders. When your ratio hits 40 percent or higher, money lenders tend to consider you too risky for a loan. You’ll have a harder time applying for car loans, student loans and mortgages.

*Ad: Clicking will take you to our partner Annuity.org.

Strategies to Pay Off Debt

Americans paid off a record $83 billion in credit card debt in 2020. The COVID-19 pandemic spurred an unexpected surge in better personal budgeting and debt elimination. Staying home, spending less, and applying stimulus checks to credit card debt were credited with the turnaround.

But it was only the second time in 35 years that Americans ended a year with less credit card debt than they started with.

Paying off your debt requires a strategy. There are several different steps to take and multiple tactics to eliminating your debt. You’ll need to consider your spending habits and behavior, plan for emergencies that can create new debt, and understand your personal psychological challenge of facing and paying off debt.

- Create a budget

- The first step is to know exactly what your income and expenses are each month. Calculate all sources of income you have coming in. Then list all your monthly expenses — rent or mortgage, utilities, transportation costs, food — any recurring expenses. Use this handy Make a Budget worksheet from the Federal Trade Commission to get started.

- Create an emergency cash reserve

- Having cash for an emergency is essential to establishing financial wellness and planning for your future retirement. Ideally, multiply your monthly expenses by three. This will tell you how much you need to save for future emergencies — especially if you lose your job. Then, make sure you and your family agree on what constitutes an emergency. That’s the only reason to dip into this fund. And any money you take out must be put back in as soon as the emergency is over.

- Pay down debt

- There are two approaches to paying off debt other than your mortgage. Both work, but some people may be more suited to one approach.

- Pay off highest interest debt first — This is the most mathematically efficient way to reduce your interest payments and save you money in the long run. But it can be psychologically challenging for some people since it can take longer to see progress.

- Pay off debts from lowest to highest — Start with the lowest balance debt, making larger payments on it until it’s paid off, then continue with each debt, paying off the highest balance debt last. This builds on your behavior and provides routine rewards as you retire debt after debt.

- Pay more than minimum monthly payments

- Pay off your target balance as quickly as possible by paying as much as you can. As you retire that debt, devote that monthly payment toward the next debt you’re paying off. This allows your money to snowball as you retire one debt after another.

- Look for balance transfers

- You likely may have to pay for a transfer, but transferring debt from a high-interest credit card to one with zero interest for several months can save you money and allow you to pay off debt.

- Control your credit cards

- If you’re not putting new purchases on your credit cards, you’re not adding debt as you try to pay them off. This will let you eliminate debt even faster. Once your debt is paid off, use credit cards only when you know you’ll pay them off almost immediately.

- Consider debt consolidation

- If you qualify, you may be able to combine your debts under a single loan payment with a lower interest rate. This may save you money in the long run. You may be able to do this through a second mortgage or a home equity loan, but you’ll have to put your home up as collateral. You could lose your home if your payments are late.

- Change your behavior

- Many people who are deeply into debt get there because of their behavior. Changing it can prevent you from slipping back into debt. Think about this as you pay off each debt, so you don’t fall back into the behavior that got you into debt to begin with. You can also add a part-time job or look for ways to cut costs — using coupons, cutting back on luxuries, joining a car pool — and devote the savings to eliminating debt.

Resources to Help You Pay Off Your Debt

There are several ways to get into seemingly unmanageable debt — medical emergencies, job loss or simply living beyond your income. But there are also resources — many of them free or at low cost — that can help you manage your debt.

- Self-help solutions

- There are several steps you can take on your own. After working out your monthly budget, stick to it. You can also contact your creditors, explain why you’re having trouble making payments, and talk about a modified payment plan. Do this as soon as you start having trouble — before your loan is turned over to a debt collector.

- Know your rights

- If your loan is purchased by a debt collector, you have certain rights under federal law — and you may have additional rights under the state laws where you live. Know your rights, and don’t let debt collectors pressure you to waive them.

- Manage home and auto loans

- Home and auto loans are typically secured loans — meaning the loans are tied to the asset, either the home or car. Car loan creditors can usually repossess your car at any time if you default on the loan. If you’re close to that point, you may be better off selling the car to pay off the loan. If you fall behind on your mortgage payments, contact your lender immediately. You may be able to temporarily reduce or delay payments if your setback is temporary — such as the loss of a job.

- Credit counseling

- Most credit counseling services are nonprofits that offer their services over the phone, online or in local offices. They can advise you on managing your money and debt as well as provide financial literacy education and other educational services. You may still have to pay for services even though they are nonprofit. Check with your state attorney general to make sure the service you choose is reputable.

- Debt management plans

- Debt management plans may help some people who are too far in debt for credit counseling to help. A debt management plan (DMP) lets you deposit money into a fund each month that a credit counseling service then uses to pay off your loans. Don’t enroll in any DMP unless a certified credit counselor has first thoroughly reviewed your financial situation and has offered customized counseling on how to manage your money. Also ask your counselor how long it will take to complete the plan; they may take 48 months or more.

- Debt settlement programs

- Typically offered by for-profit companies, debt settlement programs negotiate a settlement with your creditors — a lump-sum payment that is less than your debt. You’ll have to make a predetermined payment each month until you reach the lump-sum amount. There’s a lot of risk involved with these programs, which can negatively affect your credit score and leave you with debt and late fees even if you keep up payments into the program. Your creditors can even sue to garnish your wages if they don’t agree to the settlement in the end.

- Personal bankruptcy

- Bankruptcy can sometimes solve severe debt problems, but it leaves you with long-term and far-reaching consequences. There are two main types of personal bankruptcy.

- Chapter 13: If you have a steady income, Chapter 13 lets you keep property — your mortgaged home or a car — if the court approves your filing. The court will approve a repayment plan that pays off your debts over three to five years.

- Chapter 7: This type of bankruptcy liquidates all your assets except for exempt property — home, car, basic household items and work-related items. The court may order you to sell your nonexempt property to pay off your creditors.

Avoiding Debt Payoff Scams

Beware of scams that take advantage of people struggling with debt. There are two major types of these scams — advance-fee loans and credit repair scams. Many of these scammers use telemarketing schemes to reach people in debt.

Advance-fee loan scams guarantee that you receive a loan to pay off your debt — if you pay a scammer a fee up front. The fee varies but can run into several hundred dollars. Legitimate lenders will never guarantee a loan up front in exchange for any fee. Under federal law, a lender can only charge you a fee after you get the loan.

Credit repair scams promise to clean up your credit history for a fee. Mostly, their services consist of correcting inaccurate information in your credit report — something you can do yourself for free. If someone claims they can remove accurate — but negative — information about you, they’re lying and you’re being scammed. Federal and state laws prohibit that promise from being fulfilled.

- Association for Financial Counseling & Planning Education (AFCPE®) member

- Holds six Health Literacy certificates from the CDC

- Emmy® Award winner

Calling this number connects you to one of our trusted partners.

If you're interested in help navigating your options, a representative will provide you with a free, no-obligation consultation.

Our partners are committed to excellent customer service. They can match you with a qualified professional for your unique objectives.

We/Our Partners do not offer every plan available in your area. Any information provided is limited to those plans offered in your area. Please contact Medicare.gov or 1-800-MEDICARE to get information on all of your options.

844-359-1705Your web browser is no longer supported by Microsoft. Update your browser for more security, speed and compatibility.

If you need help pricing and building your medicare plan, call us at 844-572-0696