Life Insurance Information

Life insurance offers you a way to leave money behind for your family or loved ones after your life has ended. There are many different types of policies available that vary from what they cover to how you qualify. There is also a range of different ways life insurance can work, from death benefits to cash values.

- Written by Christian Simmons

Christian Simmons

Financial Writer

Christian Simmons is a writer for RetireGuide and a member of the Association for Financial Counseling & Planning Education (AFCPE®). He covers Medicare and important retirement topics. Christian is a former winner of a Florida Society of News Editors journalism contest and has written professionally since 2016.

Read More- Edited By

Lee Williams

Lee Williams

Senior Financial Editor

Lee Williams is a professional writer, editor and content strategist with 10 years of professional experience working for global and nationally recognized brands. He has contributed to Forbes, The Huffington Post, SUCCESS Magazine, AskMen.com, Electric Literature and The Wall Street Journal. His career also includes ghostwriting for Fortune 500 CEOs and published authors.

Read More- Financially Reviewed By

Eric Estevez

Eric Estevez

Owner of HLC Insurance Broker, LLC

Eric Estevez is a duly licensed independent insurance broker and a former financial institution auditor with more than a decade of professional experience. He has specialized in federal, state and local compliance for both large and small businesses.

Read More- Published: October 5, 2021

- Updated: June 9, 2023

- 5 min read time

- This page features 6 Cited Research Articles

- Edited By

Life Insurance Basics

Life insurance can be a complex topic that leaves many people with questions. However, there are basic terms and ideas that can help you to better understand how life insurance works and the options that are available to you.

- Factors Affecting Premiums and Costs:

- Your life insurance costs are affected by several factors from your life, such as your overall health, age and the type of policy you plan to purchase.

- Best Candidates:

- Healthy lifestyle choices and changes can have a positive effect on your premiums. Decisions like eating better to lose weight and quitting smoking can make a big difference.

- Benefits:

- The death benefit you or your family receives varies based on the type of policy and how much coverage you purchased.

- Fraud:

- Insurers can commit fraud against beneficiaries and vice versa. You can avoid fraud by not rushing through the selection process and ensuring that you are buying your policy from a legitimate source.

Types of Life Insurance

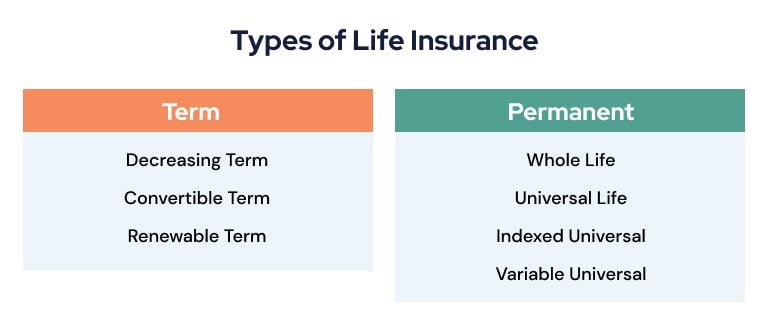

The two most common types of life insurance are term and permanent. Term life insurance provides coverage over a set amount of time, typically resulting in more affordable rates. Permanent life insurance is more expensive but offers lifelong coverage no matter when you die.

There are multiple options available for whichever type you choose to buy. Different plans may appeal to you depending on the amount of coverage that you need.

Term

- Decreasing Term:

- In this type of coverage, your death benefit steadily decreases over time. It is highest when you first buy your policy and lowest as it expires.

- Convertible Term:

- A term policy that you have the option of eventually converting into a permanent policy. Your premiums will increase since permanent life insurance is more expensive.

- Renewable Term:

- Renewable term life insurance allows you to literally renew your coverage, extending it beyond its expiration as you see fit. You can extend coverage even if you have new or worsening health problems, but your premiums can increase.

Permanent

- Whole Life:

- The most common type of permanent policy, whole life provides you with lifelong coverage. Some of your premiums also go toward cash value that can be invested or withdrawn with possible tax benefits, if structured correctly.

- Universal Life:

- This type of policy is a more flexible version of permanent life insurance. You get lifelong coverage but can alter your death benefit payout and how much you pay in premiums under certain circumstances.

- Indexed Universal:

- An indexed universal policy has a cash value that is tied to market performance as well as a death benefit. This type gives you the opportunity for a lot of growth but also comes with the inherent risk of relying on the performance of a market.

- Variable Universal:

- A variable universal policy is a combination of universal life and variable policies, offering you lifelong coverage but with investment options.

Life Insurance Companies

There are many life insurance companies that offer different plan structures and types of coverage. Before selecting a plan, it is important to do your research and learn about the options available to you.

- Quotes:

- Life insurance quotes are a look at your potential premium rate and death benefit from a company. You may want to get quotes from a few different companies or policies that you are interested in to compare rates.

- Top-Rated Companies:

- You may also want to consider some of the best life insurance companies on the market. According to the U.S. News & World Report, some of the best companies in 2021 were Northwestern Mutual, Haven Life and State Farm.

How Life Insurance Works

For a typical life insurance policy, you pay a premium while you are alive that results in a death benefit being paid out to your beneficiaries shortly after you die. However, not all policies are that simple and there are other things to consider, like cash value and tax situations.

- Death Benefit:

- The death benefit is the payout your family receives after you die. This can vary from a lump-sum payment to installments and the amount is determined by the type of policy among other factors.

- Premium:

- Your premium is the monthly fee that you pay the insurance company to keep your life insurance. The price varies by type of insurance.

- Cash Value:

- Some policies include a cash value that you can grow over the years. You can often borrow against or withdraw from this cash value.

- Beneficiaries:

- Your beneficiaries are whoever you have named on your policy to receive your death benefit once you have died. Your beneficiary is often a family member.

- Taxes:

- Life insurance payouts are generally not taxable, so your beneficiary shouldn’t owe taxes on a death benefit. There are some circumstances – like if the benefit is not received in a lump sum – that can lead to taxation.

Life Insurance Riders and Policy Changes

Life insurance riders are separate additions to your policy that can allow you to tailor your specific contract to what you value the most. There are several different types and options available.

- Types:

- Common types include an accelerated benefit rider, which provides you with benefits while you are still alive, or an accidental death rider, which increases the death benefit if you die in an accident.

- Rider Benefits:

- The benefit of adding riders to your policy is to increase your coverage or to better fit the contract to your specific situation. Riders allow you to address situations that may not be covered in a typical policy.

- Policy Restructuring:

- There are riders you can add that allow you to restructure your policy after it has begun. This allows for changes like altering your eventual death benefit or changing the type of policy you have.

- Certified educator in personal finance

- Bachelor’s degree in journalism from the University of Central Florida Burnett Honors College

- Master’s degree in integrated business from the University of Central Florida

6 Cited Research Articles

- Shelton, S., & Threewit, C. (2021, August 27). Best Life Insurance Companies of 2021. Retrieved from https://www.usnews.com/insurance/life-insurance

- Danise, A. (2021, August 24). Term Life Insurance Explained. Retrieved from https://www.forbes.com/advisor/life-insurance/choosing-the-right-term-life-insurance/

- Kilroy, A. (2020, May 20). What To Know About Cash Value Life Insurance. Retrieved from https://www.forbes.com/advisor/life-insurance/cash-value-life-insurance/

- Frailich, R. (2020, April 13). Life Insurance Riders Explained. Retrieved from https://www.forbes.com/advisor/life-insurance/riders/

- Insurance Information Institute. (n.d). How to choose the right type of life insurance. Retrieved from https://www.iii.org/article/how-choose-right-type-life-insurance

- Insurance Information Institute. (n.d). What are the different types of permanent life insurance policies? Retrieved from https://www.iii.org/article/what-are-different-types-permanent-life-insurance-policies

Your web browser is no longer supported by Microsoft. Update your browser for more security, speed and compatibility.

If you need help pricing and building your medicare plan, call us at 844-572-0696