Laddering Life Insurance Policies

The laddering insurance strategy is purchasing multiple term policies of different lengths. This way, you have the most coverage while you’re young, and premium costs decrease as each term expires. Laddering policies can be beneficial to those with nonpermanent financial goals. Learn how laddering your life insurance policy can help you reach your financial and lifestyle goals.

- Written by Lindsey Crossmier

Lindsey Crossmier

Financial Writer

Lindsey Crossmier is an accomplished writer with experience working for The Florida Review and Bookstar PR. As a financial writer, she covers Medicare, life insurance and dental insurance topics for RetireGuide. Research-based data drives her work.

Read More- Edited By

Lamia Chowdhury

Lamia Chowdhury

Financial Editor

Lamia Chowdhury is a financial content editor for RetireGuide and has over three years of marketing experience in the finance industry. She has written copy for both digital and print pieces ranging from blogs, radio scripts and search ads to billboards, brochures, mailers and more.

Read More- Financially Reviewed By

Eric Estevez

Eric Estevez

Owner of HLC Insurance Broker, LLC

Eric Estevez is a duly licensed independent insurance broker and a former financial institution auditor with more than a decade of professional experience. He has specialized in federal, state and local compliance for both large and small businesses.

Read More- Published: September 30, 2022

- Updated: June 9, 2023

- 4 min read time

- This page features 7 Cited Research Articles

- Edited By

What Is the Life Insurance Laddering Strategy?

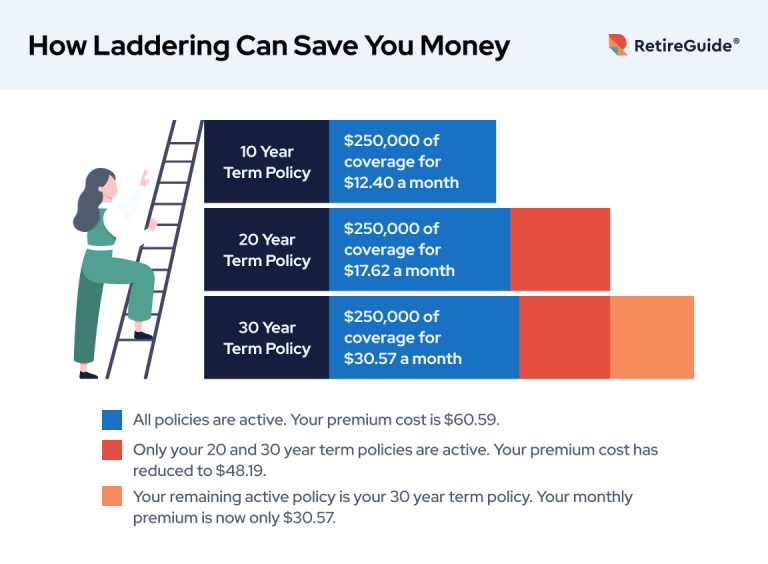

To ladder term policies, you purchase multiple term life insurance policies with different expiration dates. For example, you could buy a 30-year policy, a 20-year policy and a 10-year policy. All the policies become active at the same time, and you have the most coverage within the first 10 years.

As you age, some of your financial dependents, such as your kids, are no longer your responsibility to provide coverage for. Your premium price will become more affordable as each term policy’s coverage ends. There’s no need to spend excess money on coverage you no longer need.

How Does Laddering Save You Money?

With a term policy, your policy length and death benefit amount affect your premium costs. For example, A 30-year term policy with $750,000 of coverage is going to cost more than a 10-year term policy with $250,000 of coverage.

To save money on premiums, you could purchase a 10-year term policy, a 20-year term policy and a 30-year term policy with $250,000 of coverage each. In the end, you only must pay the premiums for $750,000 of coverage when you need it. As each term ends, your premium cost will reduce to your new financial needs.

For example, let’s say you calculated that you only need $750,000 of coverage for the next 10 years. You’re accounting for your kids, debt and mortgage.

After 10 years, your kids are grown up, you think you’ll only need $500,000 of coverage.

After 20 years, you predict you’ll only have medical bills and burial costs to cover, needing only $250,000 of coverage.

If you don’t think you need $750,000 for the entire 30-year term length, breaking up your premiums by laddering multiple policies can save you money.

How to Ladder Policy Quotes

When looking into laddering term policies, you should first consider how much coverage you need, and how long you will need each policy to be active.

- Consider how many years you’d want your lost income covered

- Determine how much debt you have

- Determine how much is remaining on your mortgage

- If you have kids, consider how much it would cost to send them to college or cover wedding costs

- Consider your funeral and health care costs

While your debt, income and health care costs may vary, there are some costs you can estimate and account for while laddering your policies. In 2021, the average wedding cost was $34,000. The average in-state college tuition and fees cost $10,338 throughout 2021 and 2022, according to U.S. News. As of August 12, 2022, the average 30-year fixed mortgage rate is 5.54%. This is a high jump compared to a 30-year fixed mortgage as of January 7, 2021, which was 2.65%. The average funeral cost is between $7,000 to $12,000.

Typically, you have more expenses to cover when you’re young. As you age, the coverage you need tapers off.

Laddering multiple policies can be complex. You could consider adding riders to add extra coverage on one term policy. There can also be administrative fees to each policy.

Having a financial advisor help you ladder your term policies can help guarantee you get the best price and right coverage amount. Make sure you compare costs from different companies before purchasing your policies.

Is Laddering Policies Right for You?

Laddering your policies could suit your financial needs if you don’t think you’ll need steady coverage for a long period. New parents or homeowners would likely benefit from laddering their policies. You’d save money in the long run by having your premium costs decrease over time.

Laddering policies could also fit your needs if you don’t know where your finances will be in 30 years or so. It’s possible that you won’t be able to afford a steady costly premium that provides ample coverage.

Inflation in 2022 has made many question their future expenses. In just 10 years, inflation has greatly affected costs. According to the U.S. Bureau of Labor Statistics, $100 in July 1992 has the same buying power as $210.87 in July 2022. If you don’t think you could afford a steady premium as inflation continues to shift, you may want to consider laddering term policies instead.

If you believe you will need full coverage throughout the entire term, you should not ladder your term policies. It will leave you unprepared to cover future expenses. If you need lifetime coverage, laddering your policies would not fit your financial goals.

- Special focus on content about life insurance, Social Security, Medicare and certificates of deposits (CDs)

- Research-based data drives her work

- Bachelor’s degree in English from the University of Central Florida

7 Cited Research Articles

- Fred Economic Data. (2022, August 18). 30-Year Fixed Rate Mortgage Average in the United States. Retrieved from https://fred.stlouisfed.org/series/MORTGAGE30US

- Stauffer, J. (2022, August 12). Today’s National Mortgage Rates, August 12, 2022 | Rates Back Above 5.5%. Retrieved from https://time.com/nextadvisor/mortgages/rates/

- The Knot. (2022, February 15). The Knot 2021 Real Weddings Study. Retrieved from https://www.theknot.com/content/wedding-data-insights/real-weddings-study

- Powell, F. & et al. (2021, September 13). See the Average College Tuition in 2021-2022. Retrieved from https://www.usnews.com/education/best-colleges/paying-for-college/articles/paying-for-college-infographic

- Progressive Casualty Insurance Company. (n.d.). How Much Does Life Insurance Cost? Retrieved from https://www.progressive.com/answers/how-much-is-life-insurance/

- U.S. Bureau of Labor Statistics. (n.d.). CPI Inflation Calculator. Retrieved from https://www.bls.gov/data/inflation_calculator.htm

- Lincoln Heritage Funeral Advantage. (n.d.). How Much Does a Funeral Cost? Retrieved from https://www.lhlic.com/consumer-resources/average-funeral-cost/

Your web browser is no longer supported by Microsoft. Update your browser for more security, speed and compatibility.

If you need help pricing and building your medicare plan, call us at 844-572-0696