Medicare Costs: Why You May Pay More for Health Care

Several factors, including age, income and health status, impact how much a Medicare beneficiary pays for health care. As federal health care expenditures rise, Medicare beneficiaries will likely see out-of-pocket costs increase in 2023 and beyond.

- Written by Rachel Christian

Rachel Christian

Financial Writer and Certified Educator in Personal Finance

Rachel Christian is a writer and researcher for RetireGuide. She covers annuities, Medicare, life insurance and other important retirement topics. Rachel is a member of the Association for Financial Counseling & Planning Education.

Read More- Edited By

Lee Williams

Lee Williams

Senior Financial Editor

Lee Williams is a professional writer, editor and content strategist with 10 years of professional experience working for global and nationally recognized brands. He has contributed to Forbes, The Huffington Post, SUCCESS Magazine, AskMen.com, Electric Literature and The Wall Street Journal. His career also includes ghostwriting for Fortune 500 CEOs and published authors.

Read More- Published: May 27, 2021

- Updated: October 13, 2023

- This page features 27 Cited Research Articles

Featured Experts

Mary Johnson, Medicare Policy Analyst with The Senior Citizens LeagueShannon Hohl, Program Supervisor at the Idaho Senior Health Insurance Benefit Advisors (SHIBA)Caitlin Donovan, Health Care Policy Expert with the Patient Advocate FoundationChristine Mahoney, Public Affairs Specialist with the U.S. Centers for Medicare & Medicaid ServicesTricia Neuman, Senior Vice President of the Kaiser Family FoundationRead their full bios below the article. - Edited By

Aline Luenebrink paid $300 each month in 2020 for her prescription drugs with Medicare.

It was a huge expense for the retiree, who receives less than $10,000 a year in Social Security benefits.

“With just my Social Security, there’s no way I can afford those prices,” the 68-year-old told RetireGuide.

Luenebrink isn’t alone.

While Medicare provides vital health care coverage to more than 62 million adults ages 65 and older as well as some younger people with disabilities, Original Medicare’s benefit design includes high cost-sharing and no limit on out-of-pocket costs.

Many Medicare beneficiaries must pay monthly premiums, meet deductibles and shoulder copays for things such as prescription drugs and outpatient care.

Some pay substantial amounts out of pocket for devices and services Medicare doesn’t cover, such as long-term care.

On average, people with Original Medicare spent $5,801 on insurance premiums and medical services, according to an AARP analysis of 2017 data.

That’s a nearly 85 percent increase from the group’s analysis of 2007 data a decade prior.

As the federal government grapples to cover escalating health care costs, new policy changes may result in higher expenses for beneficiaries.

Breaking Down Medicare Out-of-Pocket Costs

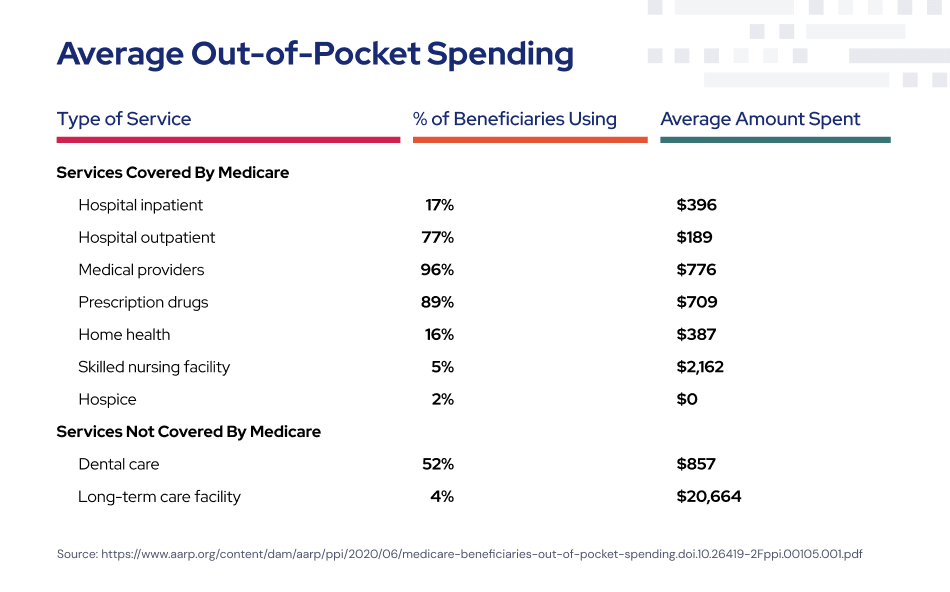

The AARP analysis of out-of-pocket costs draws data from the 2017 Medicare Current Beneficiary Survey (MCBS), an annual nationally representative survey of Medicare enrollees conducted by the U.S. Centers for Medicare & Medicaid Services (CMS).

The report shows that nearly half — 47 percent — of Original Medicare beneficiary out-of-pocket costs in 2017 went to Medicare or supplemental insurance premiums. (The AARP analysis excludes beneficiaries enrolled in private Medicare Advantage plans.)

The analysis also found that beneficiaries spent an average of $709 on prescription drugs each year along with $776 on office visits and doctor services.

The rest went to cost-sharing payments or services not covered by Original Medicare, such as dental work and long-term care.

While only 5 percent of Original Medicare beneficiaries stayed at a skilled nursing facility, those who did spent an average of $2,162 out-of-pocket in 2017.

Long-term care — which includes extended stays at nursing homes and assisted living facilities — isn’t covered by Medicare. Four percent of Original Medicare beneficiaries stayed at such facilities in 2017, where they spent an average of $20,664 out-of-pocket, according to the AARP report.

Premiums and Deductibles

Exactly how much a Medicare beneficiary pays depends on their specific coverage.

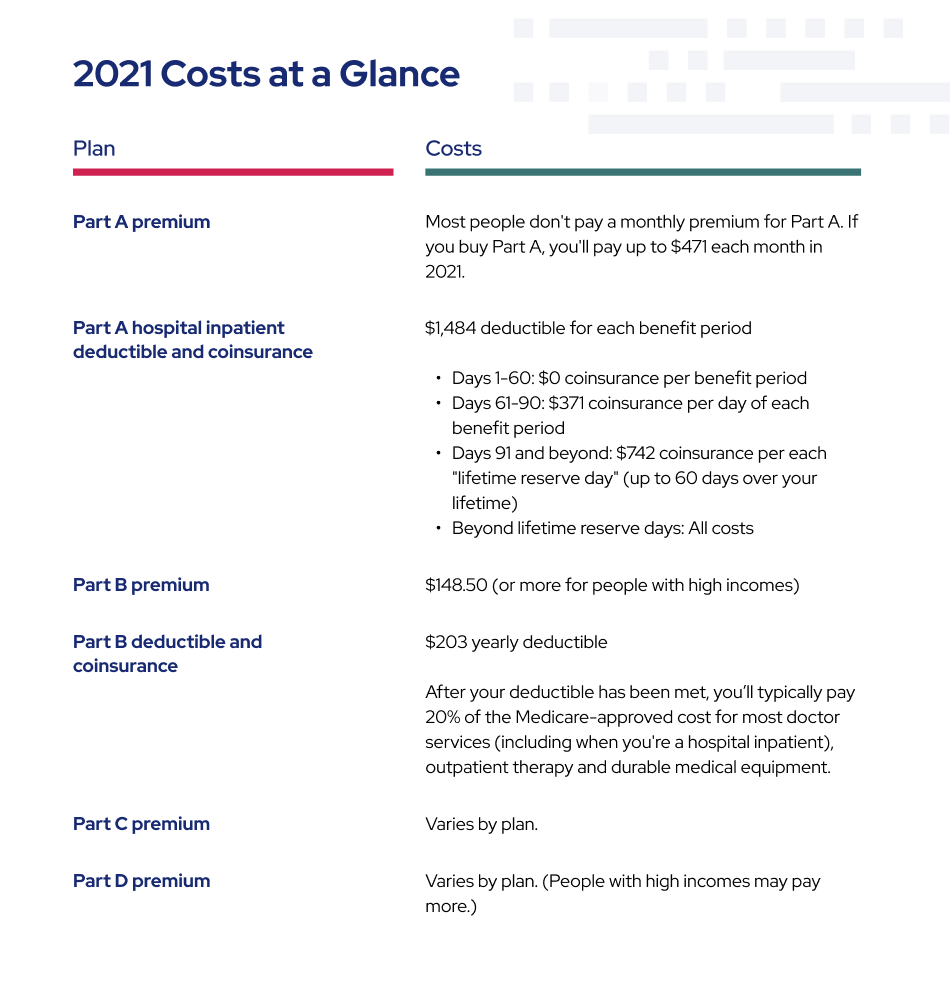

Original Medicare consists of Part A hospital insurance and Part B outpatient care. Each comes with its own costs.

Most people don’t owe a premium for Part A because they already paid for it through payroll taxes while working. But many beneficiaries owe a monthly premium of $148.50 for Part B — or $1,782 a year — in 2021.

Beneficiaries are also responsible for the $203 Part B annual deductible in 2021 and 20 percent of all doctor services and office visits.

Standalone Part D prescription drug plans administered by private companies often come with their own deductibles and monthly premiums for those who don’t qualify for low-income subsidies.

And enrollees can owe a $1,484 Part A deductible each time they’re admitted to the hospital in 2021.

The Impact of Supplemental Insurance

Supplemental insurance, such as a Medigap policy or an employer-sponsored plan, can help offset some of these costs.

“Medicare comes with unusually high levels of out-of-pocket spending that can run into the tens of thousands of dollars a year without supplemental insurance,” said Mary Johnson, a Medicare policy analyst for The Senior Citizens League, one of the nation’s largest nonpartisan advocacy groups for older Americans. “Supplements can make a big difference in the health and quality of life people enjoy in retirement.”

But while private Medigap policies limit some expenses and provide protection against catastrophic costs, Medigap premiums can be costly, ranging from $150 to about $200 a month.

The poorest Medicare beneficiaries can qualify for both Medicare and Medicaid, a designation known as dual eligible. Most health care costs are covered for these beneficiaries, but Medicaid income limits and eligibility requirements vary by state. In 2018, about 13 percent of Medicare enrollees were fully eligible for both programs.

Another 5.9 percent received some premium and cost-sharing assistance through Medicare Savings Programs, according to RetireGuide’s analysis of MCBS data from 2018, the most recent year available. These programs are designed for beneficiaries with incomes that exceed Medicaid limits but who still struggle to pay their health care bills.

“But beneficiaries on the borderline who do not qualify for these programs face the risk of running out of savings due to high health care costs,” Johnson said. “I have seen retirees over 70 years old return to work just to afford surgery.”

Over a third of all Medicare beneficiaries choose to receive their Part A and Part B benefits through a Medicare Advantage plan, which is a plan administered by a private insurance company that contracts with the federal government.

In 2020, 90 percent of Medicare Advantage plans included prescription drug coverage, and many include extra benefits — such as dental, hearing and vision — that Original Medicare doesn’t fully cover.

And unlike Original Medicare, Medicare Advantage plans are required by law to have limits on out-of-pocket costs.

About 40 percent of Medicare Advantage beneficiaries pay a premium for their plan on top of their Part B premium. This additional cost averages $63 a month, according to an analysis from the Kaiser Family Foundation.

Medicare Out-of-Pocket Costs in Relation to Income

Medicare recipients often live on fixed incomes, underscoring the financial burden felt by many beneficiaries.

Half of all enrollees had incomes below $26,200 in 2016, and the average monthly Social Security retirement benefit in 2020 was $1,514, or $18,168 a year. Social Security benefits for the disabled were even less, at $15,108 a year on average.

Such limited resources can make even modest out-of-pocket costs difficult to manage.

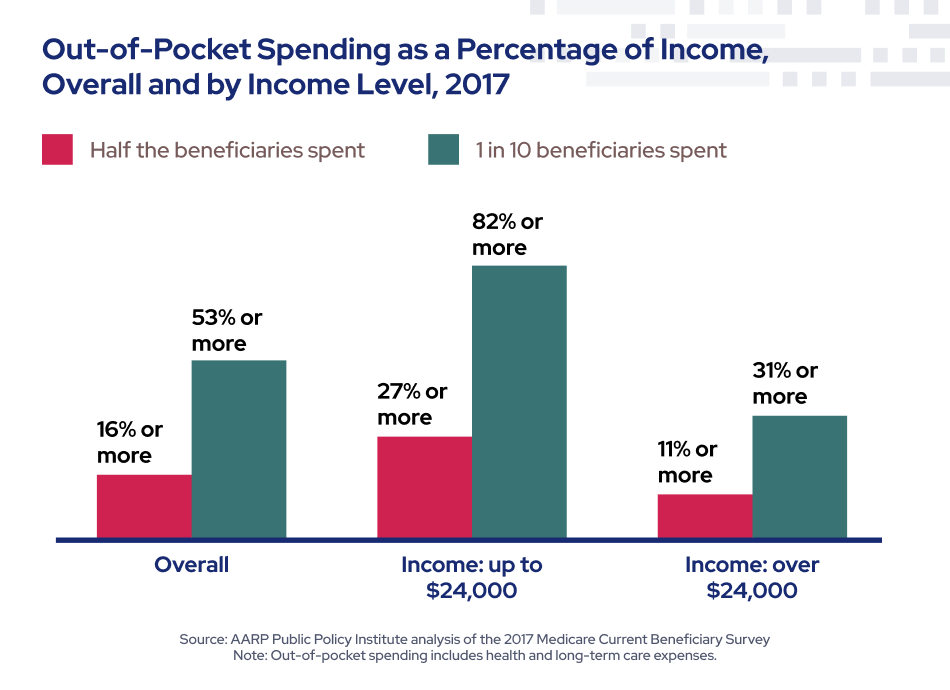

One in 10 beneficiaries spent over half their income on health care in 2017, according to the AARP report.

Half of people with incomes less than $24,120 spent 27 percent or more of their income on Medicare insurance and health care services.

In contrast, people with incomes above $24,120 spent 11 percent or more of their income.

Beneficiary Spotlight: Aline’s Story

Aline Luenebrink, like many Medicare beneficiaries, has several chronic conditions, including high blood pressure and high cholesterol.

The Indiana resident receives her health care benefits through Original Medicare. She has a supplement policy that picks up many expenses, including her copays at the doctor’s office.

She also has a workers’ compensation settlement that sets aside money for health care costs related to a workplace spinal injury.

But neither her Medicare supplement nor her workers’ comp set-aside covers her Part D out-of-pocket drug costs.

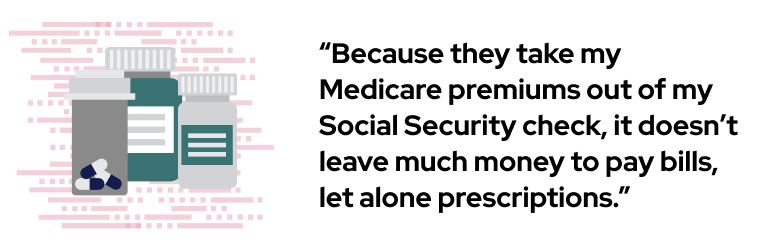

“Because they take my Medicare premiums out of my Social Security check, it doesn’t leave much money to pay my bills, let alone prescriptions,” said Luenebrink, who noted that the workers’ comp money has made it difficult to qualify for Medicaid.

After struggling for months to afford her medication, Luenebrink’s doctor told her about a closed-door pharmacy located within a nearby hospital. Closed-door pharmacies aren’t typically open to the public and can often provide medications at a lower rate than retail pharmacies.

It was cheaper for Luenebrink to get her drugs from the closed-door pharmacy without health insurance than to use her Medicare Part D plan somewhere else.

“Now thankfully I only pay about $60 a month for my medications, “Luenebrink said. “But it took a while to figure this out. It’s ridiculous my medications cost so much with Medicare. They don’t make it easy to understand why you’re paying so much or how to get it cheaper.”

Medicare Costs Increase with Age

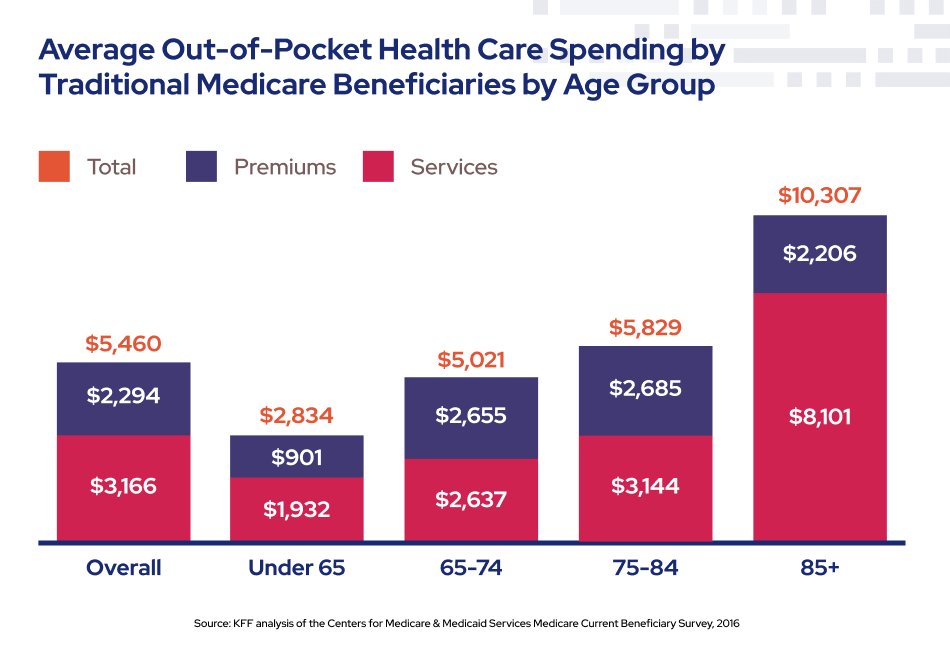

Aging is expensive. Medicare’s oldest beneficiaries — those ages 85 and older — often bear the brunt of out-of-pocket costs, due in part to expensive surgeries and long-term care costs.

People ages 85 and older spent $10,307 on average in 2016 — more than twice as much as beneficiaries between the ages of 65 and 74, according to a Kaiser Family Foundation analysis of 2016 MCBS data.

Elderly Medicare patients also allocated more income to these out-of-pocket costs than their younger counterparts.

Health care for the elderly is costly for the federal government, too.

Only 5 percent of Medicare beneficiaries die each year, but one-quarter of Medicare program spending occurs in the last year of life, according to a 2018 research paper published in the journal Science.

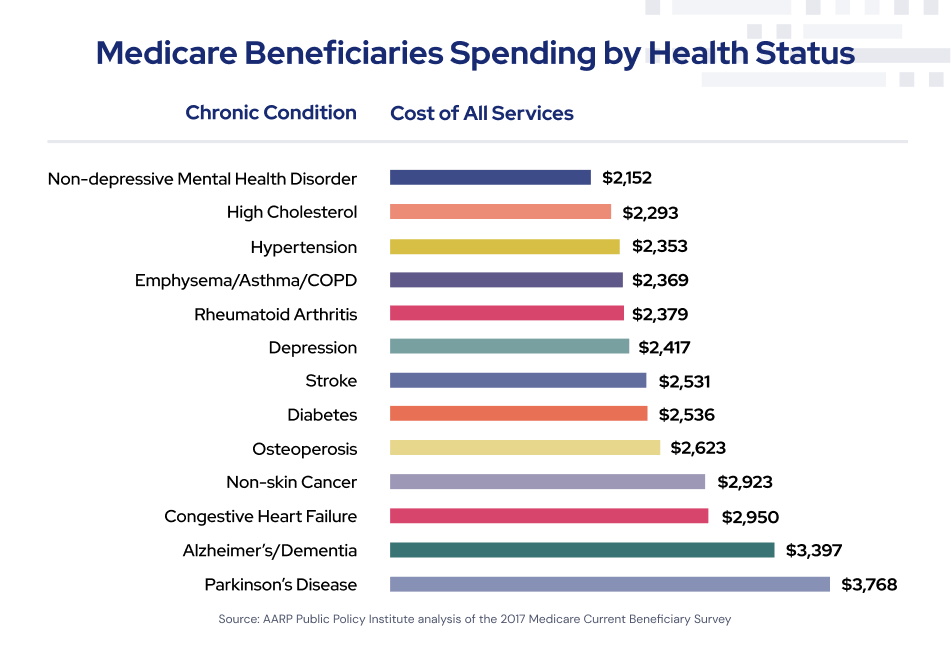

People with Multiple Chronic Conditions Face Higher Out-of-Pocket Costs

Medicare beneficiaries with one or more chronic conditions often face substantially higher out-of-pocket costs for prescription drugs, physician services and outpatient hospital care than the average beneficiary.

Almost a third — 32.5 percent — of the Medicare population reported having four to five chronic conditions in 2018.

According to an AARP analysis of 2017 MCBS data, beneficiaries in self-reported fair or poor health paid an average of $2,755 out of pocket for services — about 45 percent more than people in self-reported excellent or very good health.

Original Medicare beneficiaries with Parkinson’s disease spent more out-of-pocket annually — $3,768, on average — than enrollees with any other type of illness, according to the AARP report.

Cancer was the second costliest condition in 2017, with average spending of $3,397, followed by congestive heart failure at $2,950.

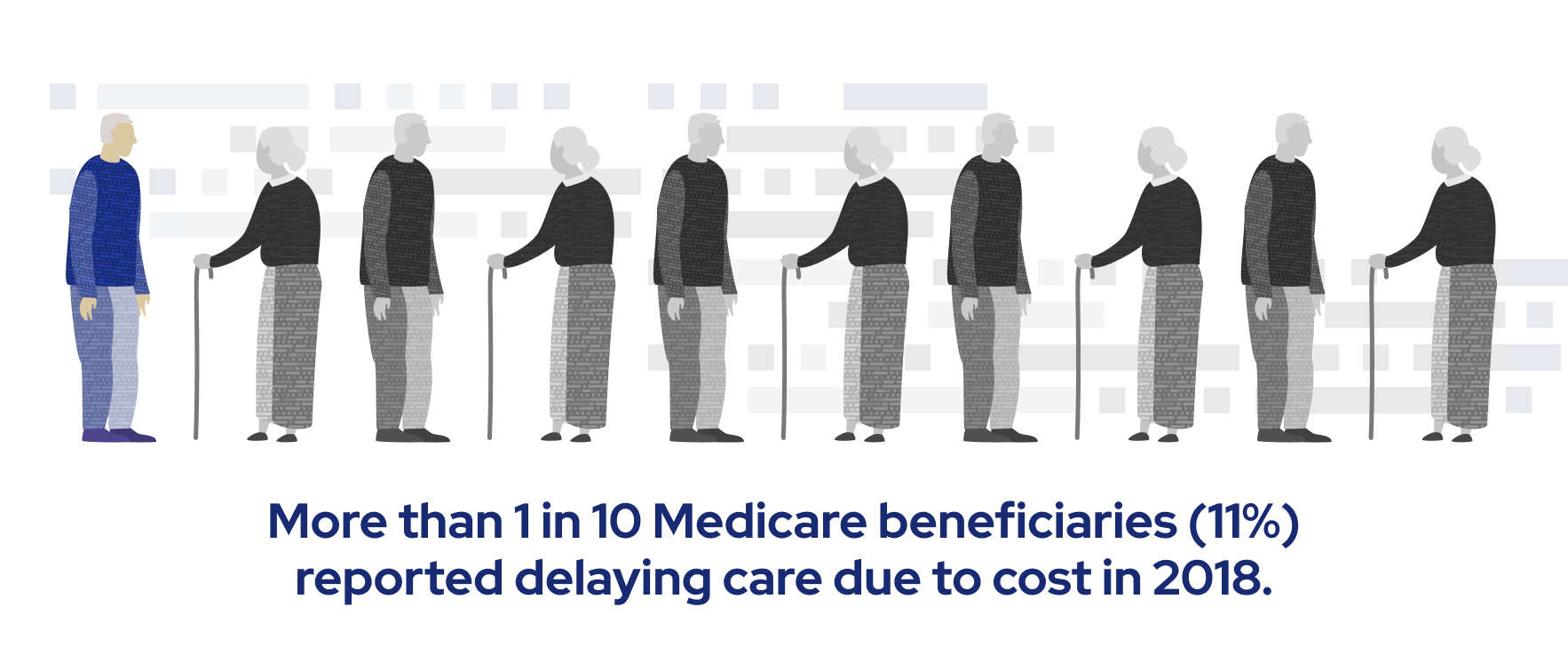

Medicare Beneficiaries Who Delay or Neglect Care Due to Cost

More than 1 in 10 Medicare beneficiaries — 11 percent — reported delaying care due to cost in 2018, according to MCBS data analyzed by RetireGuide.

Not surprisingly, beneficiaries with lower incomes are more likely to forgo care due to cost.

According to a Kaiser Family Foundation analysis of 2017 MCBS data, 26 percent of Medicare recipients with incomes under $20,000 had difficulty getting care or paying medical bills due to cost.

In contrast, just 7 percent of beneficiaries with incomes of $40,000 or higher delayed care due to cost.

The pattern held true for people enrolled in both Original Medicare and Medicare Advantage.

Ways to Reduce Out-of-Pocket Medicare Costs

While some costs are unavoidable, certain proactive steps can help Medicare beneficiaries reduce their out-of-pocket expenses.

Experts recommend reviewing your plans and coverage each year to find ways to save money.

“It’s important to consider ways to protect yourself from unexpected medical costs,” Shannon Hohl, program supervisor at the Idaho Senior Health Insurance Benefit Advisors, told RetireGuide. “Reviewing your options is one way to make sure you have coverage that works for your health and your budget.”

Each state has a free network of trained volunteers who can help beneficiaries and caregivers navigate Medicare, Medicare Advantage, Medigap and Medicaid benefits.

They’re called State Health Insurance Assistance Programs, or SHIPs, although some states use different abbreviations, such as SHIIP, SHINE, HICAP and SHIBA.

Hohl recommends that people who are concerned about Medicare costs call their local toll-free SHIP number.

“Medicare benefits and premiums change annually so it’s important for beneficiaries to review their coverage each year,” she said. “It’s the best way to ensure you have the coverage that works for you.”

How to Spot Billing Errors and Reduce Your Medicare Costs

Medical billing errors can cause high out-of-pocket sticker shock for people on Medicare.

Caitlin Donovan is a health care policy expert at the nonprofit Patient Advocate Foundation. She told RetireGuide that billing mistakes are extremely common. Her organization estimates that at least half of all patient medical bills contain errors.

“And we’ve never seen an error work in a patient’s favor,” Donovan added.

Donovan personally experienced the cost of incorrect billing when she was pregnant with her third child.

After examining each medical bill and disputing errors, she discovered mistakes in half her bills — and those discrepancies totaled about $650.

Here are some expert tips and advice to handle medical billing issues and save money on Medicare.

Caitlin Donovan is a nationally recognized health care policy expert and senior director of public relations with the Patient Advocate Foundation.

A lot of people don’t realize that Original Medicare doesn’t have an out-of-pocket max. There can also be multiple benefit periods in a year, along with multiple deductible resets if you’re admitted to the hospital multiple times in a year. This can be quite shocking to a lot of people.

There’s also the 20 percent cost sharing charge, which can really add up.

That’s why it’s important when you first sign up for Medicare to strongly consider getting a Medigap supplement policy.

If your window for that has passed, or the cost of a supplement policy is too high, keep exploring your options. A Medicare Advantage plan may be a better choice than sticking to Original Medicare without any kind of supplemental insurance.

You shouldn’t pay any [Medicare Advantage or Part D] bill until you receive your Explanation of Benefits. That’s the thick packet you receive in the mail that says “this is not a bill.”

The Explanation of Benefits is always very specific to the bill you received after each treatment or medication.

(Original Medicare beneficiaries, in contrast, receive what’s known as a Medicare Summary Notice. These are mailed out four times a year.)

One of the most common billing mistakes we see are providers billing patients directly instead of submitting through insurance. This can happen for a few reasons. For example, a provider may have a claim denied by Medicare and instead of fixing it, they just bill the patient directly, either as a mistake or intentionally.

Waiting for your EOB is a good way to make sure Medicare has received a claim from your provider and the provider has paid their share.

You can compare your bill and EOB to see what you owe, and make sure it’s the correct amount. If they’re different, there’s probably been a mistake somewhere. In that case, call your provider or insurer, depending on the mistake.

Most private insurers allow you to log in and see a copy of all your EOBs in one place.

Being organized and keeping good records can be so helpful. If you need to file an appeal, getting documentation together can be difficult if you aren’t organized.

Keep copies of EOBs and billing statements. You should also keep documents that may come from a doctor, especially if you go through prior authorization. And hold onto anything to do with your Part D plan.

We always recommend patients keep a file with these documents for about a year, just in case.

A good example of when to talk to Medicare first is asking why something was denied.

Oftentimes, you don’t need to go through the appeals process because the issue may be as simple as incorrect coding by the provider who needs to re-submit the claim. A claim can even get denied because the address the provider submitted is different from what Medicare has on file.

Once you find out from Medicare why a claim was denied, you still usually need to go back to the provider and play a game of telephone. But it’s ultimately worth it. We see so many mistakes and billing errors every day, and these mistakes add up.

Take a look at what you’re paying now and your average yearly out-of-pocket costs. Prescriptions are usually a big cost for people on Medicare.

Your pharmacist can be really helpful in determining ways to reduce your prescription costs. They usually have a list of all your medications, assuming you get them filled with the same company.

Your pharmacist can let you know about discounts, or if cheaper generics are available.

You should also ask your doctor if you still need all the medications you’re prescribed. You may not need certain drugs anymore and eliminating those can save you money.

Last year, it took our experts about 17 phone calls to resolve each case. We get more complex cases than just an incorrect address, but that gives you an idea of how time consuming this can be.

As you get older and your conditions become more complex, mistakes can add up quickly. It’s really important to stay on top of it because unfortunately, your physical and fiscal health are intimately connected.

Making sure you’re not overpaying for your health while getting your insurance to pay what it’s supposed to is really vital.

What Causes the Government to Raise Medicare Prices?

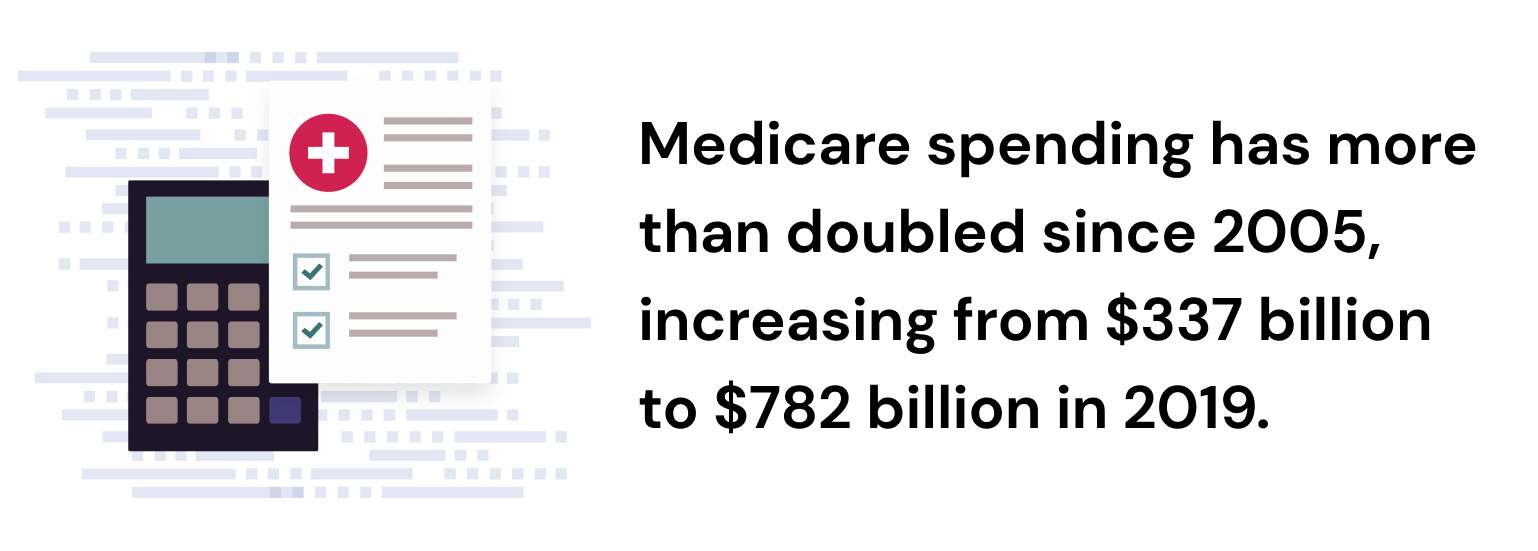

Millions of Americans face out-of-pocket Medicare costs, but these expenses are a fraction of what the federal government pays to provide health care for each beneficiary.

Medicare spending has more than doubled since 2005, increasing from $337 billion to $782 billion in 2019.

The aging baby boomer generation has also accelerated Medicare enrollment growth over the last decade.

Total Medicare program spending over the next 10 years is projected to rise an average of 7 percent per year, according to the Medicare Payment Advisory Commission, a nonpartisan legislative agency that provides the U.S. Congress with analysis and policy advice.

As enrollment and health care costs rise, experts say Medicare spending will continue to climb.

High costs that exceed revenue have put the Medicare Hospital Insurance (HI) Trust Fund in financial jeopardy.

The trust fund, which pays for hospital and other inpatient care, is financed primarily by payroll taxes. But that money — as well as other smaller sources of revenue — isn’t sufficient to pay the bills.

Medicare Part B, which pays for doctor visits and other outpatient costs, is funded by beneficiary premiums and appropriations by Congress, so it cannot technically become insolvent.

In April 2020, Medicare’s annual trustees report noted that the Part A Trust Fund will begin to run out of money by 2026 — just five years from now.

A more recent projection from the Congressional Budget Office, or CBO, also estimated depletion of the fund in 2026.

An anticipated $517 billion in spending reductions and/or additional revenue will be necessary to cover the total trust fund deficit between 2026 and 2031, according to CBO projections.

In the last three decades, the Medicare HI trust fund has only come within five years of depletion twice — in 1996 and 1997.

Lawmakers have never allowed the fund to become fully depleted.

To prevent a shortfall in 2026, the government will need to act. Experts say a few things could happen.

Premiums and Medicare payroll taxes may rise. Specifically, the standard 2.9 percent Medicare payroll tax — which hasn’t changed in 35 years — would need to immediately increase to 3.66 percent.

Alternatively, payments to doctors, hospitals and other health care providers could be cut while Medicare benefits are trimmed. These measures would need to slash program spending by 16 percent.

“More realistically, the tax and/or benefit changes could occur gradually,” Christine Mahoney, a CMS public affairs specialist, told RetireGuide.

But Mahoney noted that a gradual approach will require more dramatic adjustments down the road.

“Lawmakers have many options to address the long-range financial imbalance,” Mahoney said.

Upcoming Changes to Medicare’s Inpatient and Outpatient Covered Surgeries

Beneficiaries may feel another squeeze to their pocketbooks following a rule change that reclassifies Medicare payment rates for surgeries.

In December 2020, CMS finalized a significant policy change aimed at eliminating what’s known as the Medicare “inpatient only” list.

This list, which is updated yearly, identifies over 1,700 procedures that are only eligible for Medicare reimbursement if they take place in a hospital on an inpatient basis, rather than on an outpatient basis or at an outpatient clinic.

The inpatient only list is scheduled to be phased out gradually between now and the end of 2023.

Some changes have already gone into effect. As of Jan. 1, 2021, all 266 musculoskeletal-related procedures — including amputations and other high-risk surgeries — had been dropped from the list.

In theory, eliminating the list allows patients and their doctors to decide whether a surgery should take place at an outpatient clinic or an inpatient, full-service hospital.

The reclassification could also save Medicare money because CMS pays less for outpatient services.

But several policy groups and medical experts are pushing back on the decision. They warn that the most significant change may be a bigger price tag for beneficiaries.

“The shift could expose patients to substantially higher out-of-pocket costs for the same procedure,” Tricia Neuman, a Medicare policy expert and senior vice president of the Kaiser Family Foundation, told RetireGuide. “This could be a significant expense for the 5 million people covered by Medicare with no supplemental insurance.”

That’s because Medicare covers inpatient hospital stays differently from outpatient hospital stays.

Medicare patients admitted to the hospital typically receive an all-inclusive package of services through Medicare Part A. Patients must meet the Part A deductible ($1,484 in 2021) for a stay of up to 60 days, along with a 20 percent coinsurance payment for doctors’ charges. Medicare covers the rest.

In contrast, outpatient services are covered under Medicare Part B, which requires beneficiaries to pay 20 percent of the Medicare-approved amount for each service.

Charges can quickly add up for complex surgeries that may require X-rays, blood transfusions and other separately billed items.

-Tricia Neuman, Medicare policy expert and senior vice president of the Kaiser Family Foundation

There’s also a 20 percent charge for the outpatient surgery itself as well as the 20 percent share for doctors’ services.

Additional costs, including excess charges and facility fees, can also apply.

“There’s a real risk of beneficiaries paying a lot more for the same surgery, simply because of this shift from Part A to Part B,” Neuman said.

Neuman added that the new policy could also limit a patient’s care after they leave the hospital.

“If the surgery is not considered to be inpatient, the patient would not be eligible for follow-up post-acute care in a skilled nursing facility,” Neuman said.

Since the Trump administration enacted the new policy, it’s unclear if the current administration will reverse the rule before it fully rolls out in 2023.

- Member of the Association for Financial Counseling & Planning Education

- Certified educator in personal finance

- Former member of the American Finance Association

Featured Experts

-

Mary Johnson Medicare Policy Analyst with The Senior Citizens League Mary Johnson is a Social Security and Medicare policy analyst and writer for The Senior Citizens League, one of the nation's largest nonpartisan senior advocacy groups. Mary also frequently volunteers as a Medicare open enrollment benefits counselor for neighbors, friends and family.

Mary Johnson Medicare Policy Analyst with The Senior Citizens League Mary Johnson is a Social Security and Medicare policy analyst and writer for The Senior Citizens League, one of the nation's largest nonpartisan senior advocacy groups. Mary also frequently volunteers as a Medicare open enrollment benefits counselor for neighbors, friends and family. -

Shannon Hohl Program Supervisor at the Idaho Senior Health Insurance Benefit Advisors (SHIBA) Shannon Hohl has been the program supervisor of Idaho’s Senior Health Insurance Benefit Advisors (SHIBA) since 2014. She oversees a network of trained volunteers who provide free, unbiased information about health insurance to Medicare beneficiaries.

Shannon Hohl Program Supervisor at the Idaho Senior Health Insurance Benefit Advisors (SHIBA) Shannon Hohl has been the program supervisor of Idaho’s Senior Health Insurance Benefit Advisors (SHIBA) since 2014. She oversees a network of trained volunteers who provide free, unbiased information about health insurance to Medicare beneficiaries. -

Caitlin Donovan Health Care Policy Expert with the Patient Advocate Foundation Caitlin Donovan is a nationally recognized health care policy expert and senior director of public relations with the Patient Advocate Foundation. She’s been quoted in the The New York Times, The Wall Street Journal, CNN and other national media outlets. She previously served as a Washington D.C. staffer for former Congressman Gary Ackerman and former House Majority Leader Dick Gephardt.

Caitlin Donovan Health Care Policy Expert with the Patient Advocate Foundation Caitlin Donovan is a nationally recognized health care policy expert and senior director of public relations with the Patient Advocate Foundation. She’s been quoted in the The New York Times, The Wall Street Journal, CNN and other national media outlets. She previously served as a Washington D.C. staffer for former Congressman Gary Ackerman and former House Majority Leader Dick Gephardt. -

Christine Mahoney Public Affairs Specialist with the U.S. Centers for Medicare & Medicaid Services Christine Mahoney is a public affairs specialist with the U.S. Centers for Medicare & Medicaid Services, where she plans and implements communications about CMS regulations and policies. She previously served as a public relations specialist for the U.S. Navy Bureau of Medicine and Surgery as well as Defense Information Systems Agency.

Christine Mahoney Public Affairs Specialist with the U.S. Centers for Medicare & Medicaid Services Christine Mahoney is a public affairs specialist with the U.S. Centers for Medicare & Medicaid Services, where she plans and implements communications about CMS regulations and policies. She previously served as a public relations specialist for the U.S. Navy Bureau of Medicine and Surgery as well as Defense Information Systems Agency. -

Tricia Neuman Senior Vice President of the Kaiser Family Foundation Tricia Neuman is the senior vice president of the Henry J. Kaiser Family Foundation (KFF) and Executive Director of KFF’s Program on Medicare Policy, where she oversees analysis and research related to health care coverage for aging Americans and people with disabilities. Neuman has authored numerous papers on Medicare and has presented expert testimony before Congressional committees.

Tricia Neuman Senior Vice President of the Kaiser Family Foundation Tricia Neuman is the senior vice president of the Henry J. Kaiser Family Foundation (KFF) and Executive Director of KFF’s Program on Medicare Policy, where she oversees analysis and research related to health care coverage for aging Americans and people with disabilities. Neuman has authored numerous papers on Medicare and has presented expert testimony before Congressional committees.

27 Cited Research Articles

- Jaffe, S. (2021, March 21). New cost-cutting Medicare rule may add costs to patients. Retrieved from https://www.washingtonpost.com/health/new-cost-cutting-medicare-rule-may-add-costs-to-patients/2021/03/19/1197a3de-8747-11eb-8a8b-5cf82c3dffe4_story.html

- Cubanski, J. and Neuman, T. (2021, March 16). FAQs on Medicare Financing and Trust Fund Solvency. Retrieved from https://www.kff.org/medicare/issue-brief/faqs-on-medicare-financing-and-trust-fund-solvency/

- Bosco, J. (2021, February 16). CMS inpatient only policy threatens patient access to appropriate surgical setting. Retrieved from https://www.healthcaredive.com/news/cms-inpatient-only-policy-threatens-patient-access-to-appropriate-surgical/595040/

- Freed, M., Damico, A. and Neuman, T. (2021, January 13). A Dozen Facts About Medicare Advantage in 2020. Retrieved from https://www.kff.org/medicare/issue-brief/medicare-advantage-in-2022-enrollment-update-and-key-trends/

- Bunis, D. (2021, January 1). How Much Does Medicare Cost? Retrieved from https://www.aarp.org/health/medicare-insurance/info-2018/out-of-pocket-prescription-costs.html

- Rovner, J. (2020, July 21). Another Problem On The Health Horizon: Medicare Is Running Out Of Money. Retrieved from https://www.npr.org/sections/health-shots/2020/07/21/893321220/another-problem-on-the-health-horizon-medicare-is-running-out-of-money

- Noel-Miller, C. (2020, June). Medicare Beneficiaries’ Out-of-Pocket Spending For Health Care. Retrieved from https://www.aarp.org/content/dam/aarp/ppi/2020/06/medicare-beneficiaries-out-of-pocket-spending.doi.10.26419-2Fppi.00105.001.pdf

- Cubanski, J., Neuman, T. and Damico, A. (2020, April 2). Problems Getting Care Due to Cost or Paying Medical Bills Among Medicare Beneficiaries. Retrieved from https://www.kff.org/coronavirus-covid-19/issue-brief/problems-getting-care-due-to-cost-or-paying-medical-bills-among-medicare-beneficiaries/

- Congressional Budget Office. (2020). The Outlook for Major Federal Trust Funds: 2020 to 2030. Retrieved from https://www.cbo.gov/publication/56541

- Social Security Administration. (2020). Fact Sheet. Retrieved from https://www.ssa.gov/news/press/factsheets/basicfact-alt.pdf

- U.S. Centers for Medicare & Medicaid Services. (2020). 2020 Annual Report of the Boards of Trustees of the Federal Hospital Insurance and Federal Supplementary Medical Insurance Trust Funds. Retrieved from https://www.cms.gov/files/document/2020-medicare-trustees-report.pdf

- U.S. Centers for Medicare & Medicaid Services. (2020). MCBS Public Use File. Retrieved from https://www.cms.gov/Research-Statistics-Data-and-Systems/Downloadable-Public-Use-Files/MCBS-Public-Use-File

- U.S. Centers for Medicare & Medicaid Services. (2020). Medicare Current Beneficiary Survey (MCBS). Retrieved from https://www.cms.gov/Research-Statistics-Data-and-Systems/Research/MCBS

- Cubanski, J., Koma, W., Damico, A., et al. (2019, November 4). How Much Do Medicare Beneficiaries Spend Out of Pocket on Health Care? Retrieved from https://www.kff.org/medicare/issue-brief/how-much-do-medicare-beneficiaries-spend-out-of-pocket-on-health-care/

- U.S. Centers for Medicare & Medicaid Services. (2019). National Health Expenditures 2019 Highlights. Retrieved from https://www.cms.gov/files/document/highlights.pdf

- Einav, L., Finkelstein, A., Mullainathan, S., et al. (2018, June 29). Predictive modeling of U.S. health care spending in late life. Retrieved from https://www.science.org/doi/10.1126/science.aar5045

- Gleckman, H. (2018, June 6). No, Medicare Won't Go Broke In 2026. Yes, It Will Cost A Lot More Money. Retrieved from https://www.forbes.com/sites/howardgleckman/2018/06/06/no-medicare-wont-go-broke-in-2026-yes-it-will-cost-a-lot-more-money/?sh=2e5ee5ac7eb1

- U.S. Centers for Medicare & Medicaid Services. (2018). 2018 Medicare Current Beneficiary Survey Annual Chartbook and Slides. Retrieved from https://www.cms.gov/research-statistics-data-and-systemsresearchmcbsdata-tables/2018-medicare-current-beneficiary-survey-annual-chartbook-and-slides

- Commonwealth Fund. (2017, May 12). Medicare Beneficiaries’ High Out-of-Pocket Costs: Cost Burdens by Income and Health Status. Retrieved from https://www.commonwealthfund.org/publications/issue-briefs/2017/may/medicare-beneficiaries-high-out-pocket-costs-cost-burdens-income

- Jacobson, G., Griffin, S., Neuman, T., et al. (2017, April 21). Income and Assets of Medicare Beneficiaries, 2016-2035. Retrieved from https://www.kff.org/medicare/issue-brief/income-and-assets-of-medicare-beneficiaries-2016-2035/

- Medicare Payment Advisory Commission. (n.d.). National health care and Medicare spending. Retrieved from https://www.medpac.gov/wp-content/uploads/import_data/scrape_files/docs/default-source/data-book/july2021_medpac_databook_sec.pdf

- Medicare.gov. (n.d.). How is Medicare funded? Retrieved from https://www.medicare.gov/about-us/how-is-medicare-funded

- Medicare.gov. (n.d.). Medicare costs at a glance. Retrieved from https://www.medicare.gov/basics/costs/medicare-costs

- Medicare.gov. (n.d.). Medicare Savings Programs. Retrieved from https://www.medicare.gov/basics/costs/help/medicare-savings-programs

- Medicare.gov. (n.d.). What's Medicare Supplement Insurance (Medigap)? Retrieved from https://www.medicare.gov/supplements-other-insurance/whats-medicare-supplement-insurance-medigap

- The Tax Foundation. (n.d.). Social Security and Medicare Tax Rates, Calendar Years 1937 – 2009. Retrieved from https://files.taxfoundation.org/legacy/docs/soc_security_rates_1937-2009-20090504.pdf

- U.S. Centers for Medicare & Medicaid Services. (n.d.). Helping people in Medicare Advantage & Medicare Prescription Drug Plans understand their “Explanation of Benefits” (EOB). Retrieved from https://www.cms.gov/Outreach-and-Education/Outreach/Partnerships/downloads/11234-P.pdf

Calling this number connects you to one of our trusted partners.

If you're interested in help navigating your options, a representative will provide you with a free, no-obligation consultation.

Our partners are committed to excellent customer service. They can match you with a qualified professional for your unique objectives.

We/Our Partners do not offer every plan available in your area. Any information provided is limited to those plans offered in your area. Please contact Medicare.gov or 1-800-MEDICARE to get information on all of your options.

888-694-0290Your web browser is no longer supported by Microsoft. Update your browser for more security, speed and compatibility.

If you need help pricing and building your medicare plan, call us at 844-572-0696