Capital Gains Tax for People Over 65

For individuals over 65, capital gains tax applies at 0% for long-term gains on assets held over a year and 15% for short-term gains under a year. Despite age, the IRS determines tax based on asset sale profits, with no special breaks for those 65 and older. It's essential to understand these rates and any potential exemptions when planning asset sales.

- Written by Terry Turner

Terry Turner

Senior Financial Writer and Financial Wellness Facilitator

Terry Turner has more than 35 years of journalism experience, including covering benefits, spending and congressional action on federal programs such as Social Security and Medicare. He is a Certified Financial Wellness Facilitator through the National Wellness Institute and the Foundation for Financial Wellness and a member of the Association for Financial Counseling & Planning Education (AFCPE®).

Read More- Edited By

Savannah Pittle

Savannah Pittle

Senior Financial Editor

Savannah Pittle is a professional writer and content editor with over 16 years of professional experience across multiple industries. She has ghostwritten for entrepreneurs and industry leaders and been published in mediums such as The Huffington Post, Southern Living and Interior Appeal Magazine.

Read More- Reviewed By

Ebony J. Howard, CPA

Ebony J. Howard, CPA

Credentialed Tax Expert at Intuit

Ebony J. Howard is a certified public accountant and freelance consultant with a background in accounting, personal finance, and income tax planning and preparation. She specializes in analyzing financial information in the health care, banking and real estate sectors.

Read More- Published: March 21, 2023

- Updated: March 21, 2025

- 8 min read time

- This page features 14 Cited Research Articles

- Edited By

- You must pay capital gains on profits from investments.

- Long-term gains — gains from assets you’ve held for more than one year — are taxed at a maximum rate of 20%.

- Short-term gains — money generated from assets you’ve sold after owning them for less than one year — get taxed at your particular ordinary income tax rate.

- You can reduce your capital gains tax liability with several strategies, including tax-loss harvesting, charitable giving and estate planning.

What Is a Capital Gains Tax?

Capital gains taxes get levied on profits generated when you sell an asset for more money than you paid for it. Assets can be anything from stocks and bonds to real estate, jewelry, cars and collectibles like art or coins.

Because many people finance some of their retirement by selling assets they accumulated, learning how to make capital gains taxes work to your advantage can be an important aspect of retirement planning.

If your capital losses exceed your capital gains, you can use the excess loss up to $3,000 ($1,500 if married filing separately) to offset your ordinary taxable income. Any remaining loss can be carried forward into later years.

Types of Capital Gains

There are two primary types of capital gains: realized and unrealized. You only pay taxes on realized capital gains.

Realized capital gains are profits from the sale of assets. For example, if you sell a $100 stock that doubled in price (to $200) while you owned it, you have $100 in realized capital gains. At the end of the year, you’ll owe capital gains tax on that $100.

Unrealized capital gains are profits from assets you still own. For example, if you purchased a vacation home for $200,000 and now it’s worth $400,000, you have $200,000 in unrealized capital gains. But because you still own it, you won’t owe any tax on that $200,000 gain. You will owe capital gains taxes after you sell it, assuming you sell it for a profit.

The IRS also divides capital gains into two subcategories: short-term gains and long-term gains.

Short-Term Gains

Short-term gains are profits from assets owned for less than a year. An example is income made from day-trading stocks.

The IRS taxes short-term capital gains more heavily than long-term gains. Depending on your income, you could pay as much as 37% on short-term gains. IRS data shows retirees are unlikely to have many short-term capital gains to worry about.

Long-Term Gains

Long-term gains come from profits on assets owned for longer than one year. An example of this is the profits realized from selling a house that you owned for 20 years.

Many of the assets you’ll use to fund your retirement will provide long-term gains. These profits get taxed at a maximum rate of 20%, making them potentially more lucrative than their short-term counterparts.

*Ad: Clicking will take you to our partner Annuity.org.

Capital Gains Taxes and Retirement Accounts

The IRS considers retirement accounts assets, but the most common types of retirement accounts don’t incur capital gains taxes.

- Withdrawals from IRA and 401(k) accounts get taxed at your ordinary income tax level, not as capital gains.

- The same is true for profits realized from Simplified Employee Pension accounts, which are retirement vehicles for people who are self-employed. Contributions to SEP IRAs come from pre-tax money, and the IRS levies its tax when money gets withdrawn.

- Because you fund any Roth IRAs and Roth 401(k)s with after-tax income, you’ll have no capital gains or income taxes charged on withdrawals.

However, you will pay capital gains taxes on the sale of stocks and mutual funds that are not part of a designated retirement account.

Strategies for Reducing Capital Gains Taxes in Retirement

Unlike the OASDI tax, you don’t benefit from paying more capital gains tax. You’ll want to minimize the amount of these taxes as much as possible, especially if your income declines during retirement.

- Tax-Loss Harvesting

- By selling some assets at a loss, you offset gains you’ve made and reduce your tax bill for the year. The strategy comes into play if you believe your investment won’t ever turn a profit.

- Charitable Giving

- Appreciated assets you gift to charity don’t count toward capital gains taxes. You can give cash or other assets to charity and generate tax credits that will offset the capital gains taxes you owe.

- Gifting Appreciated Assets

- If you gift assets to your heirs, you won’t have to pay capital gains tax on those assets, either. The tax burden falls to your heirs, who will have to pay capital gains taxes if they ever sell the asset.

- Estate Planning

- When you leave an asset to someone in your will, no capital gains taxes get attached. If your heirs sell it later, they’ll only owe capital gains tax on the difference between its value at the time of sale and its value when they acquired it.

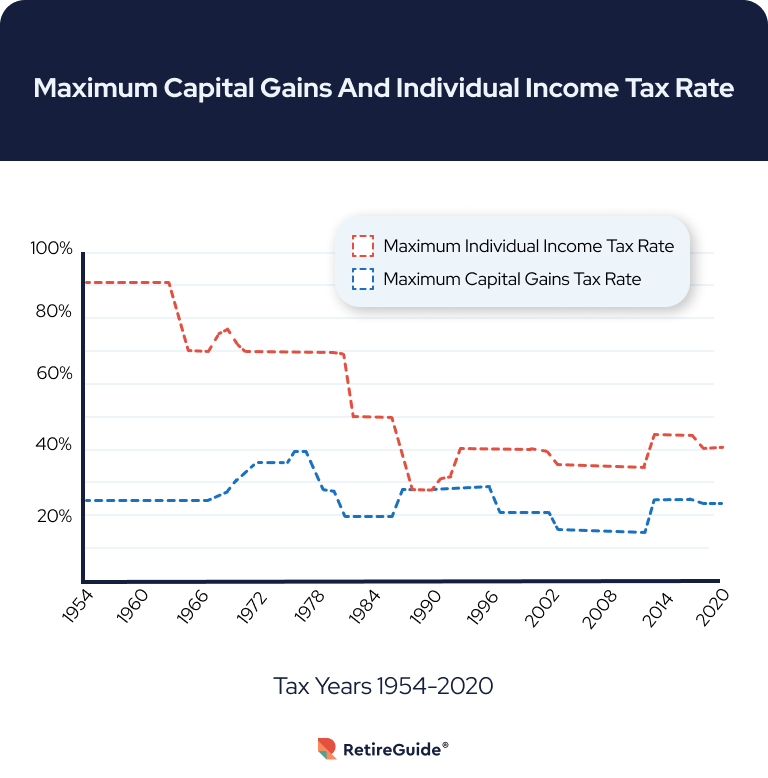

Capital Gains Tax Rates for 2022 and 2023

Your capital gains tax rate depends on your income during the year in which gains were realized. According to current IRS regulations, the higher your income, the more you pay. Rates vary for single people, married people and heads of households. Capital gains tax rates are currently capped at 20%.

| Tax Rate | Single Income | Married Filing Jointly Income | Head of Household Income | Married Filing Separately Income |

|---|---|---|---|---|

| 0% | $0 to $41,675 | $0 to $83,350 | $0 to $55,800 | $0 to $41,675 |

| 15% | $41,675 to $459,750 | $83,350 to $517,200 | $55,800 to $488,500 | $41,675 to $258,600 |

| 20% | $459,750 and above | $517,200 and above | $488,500 and above | $258,600 and above |

| Tax Rate | Single Income | Married Filing Jointly Income | Head of Household Income | Married Filing Separately Income |

|---|---|---|---|---|

| 0% | $0 to $44,625 | $0 to $89,250 | $0 to $59,750 | $0 to 44,625 |

| 15% | $44,625 to $492,300 | $89,250 to $553,850 | $59,750 to $523,050 | $44,625 to $276,900 |

| 20% | $492,300 and above | $553,850 and above | $523,050 and above | $276,900 and above |

The tax rate on short-term gains is the same as your ordinary income tax rate. This could be anywhere from 0% to 37%, depending on your income.

*Ad: Clicking will take you to our partner Annuity.org.

How To Calculate Your Capital Gains Tax Liability

It’s a good idea to pre-calculate how much you’ll owe in capital gains taxes anytime you sell an asset. Armed with this information, you can set aside some proceeds to pay the tax at the end of the year.

- Determine your cost basis. Your cost basis is the amount you paid for the asset, including fees and commissions. You’ll need to know your cost basis to calculate your gains or losses.

- Determine the sale price. The sale price is the amount you received for the asset.

- Calculate your capital gain or loss. Subtract your cost basis from the sale price. If the result is positive, you have a capital gain. If the result is negative, you have a capital loss.

- Determine if the gain is short-term or long-term: If you held the asset for one year or less, it’s a short-term capital gain. If you held the asset for longer, it’s considered a long-term gain.

- Apply the appropriate tax rate. Short-term capital gains are taxed at your ordinary income tax rate, while long-term capital gains are taxed according to the table above.

- Consider any deductions or credits. You may offset your capital gains with capital losses from other investments or claim tax credits that can lower your tax liability.

Once you determine your capital gains tax status, you’ll have to report any gains (or losses) on your annual federal tax return. The realized gains get placed on Schedule D of your return. You’ll also have to supply any relevant supporting documentation.

Consult with a Tax Professional

If your retirement plan includes selling any of your assets, you’ll likely owe capital gains taxes at some point. That’s why it’s a good idea to speak to a tax professional when you start planning (and saving) for retirement.

A qualified tax professional can determine the best way to finance the retirement lifestyle you want while minimizing the capital gains taxes. With help, you’ll make the most of the assets you’ve worked so hard to earn.

Frequently Asked Questions About Capital Gains Taxes

Connect With a Financial Advisor Instantly

Our free tool can help you find an advisor who serves your needs. Get matched with a financial advisor who fits your unique criteria. Once you’ve been matched, consult for free with no obligation.

- Association for Financial Counseling & Planning Education (AFCPE®) member

- Holds six Health Literacy certificates from the CDC

- Emmy® Award winner

14 Cited Research Articles

- Internal Revenue Service. (2023, January 26). Topic No. 409 Capital Gains and Losses. Retrieved from https://www.irs.gov/taxtopics/tc409

- Internal Revenue Service. (2023, January 19). Instructions for Schedule D (Form 1120-S) (2022). Retrieved from https://www.irs.gov/instructions/i1120ssd

- Internal Revenue Service. (2023, January 5). SEP Plan FAQs. Retrieved from https://www.irs.gov/retirement-plans/retirement-plans-faqs-regarding-seps

- Social Security Administration. (2023, January 3). What is the maximum Social Security retirement benefit payable? Retrieved from https://faq.ssa.gov/en-us/Topic/article/KA-01897

- Internal Revenue Service. (2022, December 21). Find Information on Complex Tax Topics. Retrieved from https://www.irs.gov/help/find-information-on-complex-tax-topics

- Internal Revenue Service. (2022, Oct 18). Part III Administrative, Procedural, and Miscellaneous Rev. Proc. 2022-38. Retrieved from https://www.irs.gov/pub/irs-drop/rp-22-38.pdf

- Cornell Law School Legal Information Institute. (2022, August). Capital gains. Retrieved from https://www.law.cornell.edu/wex/capital_gains

- Internal Revenue Service. (2022, July 25). 2022 Instructions for Schedule D. Retrieved from https://www.irs.gov/pub/irs-pdf/i1040sd.pdf

- Baldridge, R. and Schmidt, J. (2022, April 22). Can Tax Loss Harvesting Improve Your Investing Returns? Retrieved from https://www.forbes.com/advisor/investing/tax-loss-harvesting/

- Congressional Research Service. (2020, June 26). The Charitable Deduction for Individuals: A Brief Legislative History. Retrieved from https://sgp.fas.org/crs/misc/R46178.pdf

- University of Minnesota Extension. (2018). Gifting assets in estate planning. Retrieved from https://extension.umn.edu/transfer-and-estate-planning/gifting-assets

- International Monetary Fund. (n.d.). Realized and unrealized revaluation gains and losses. Retrieved from https://www.elibrary.imf.org/downloadpdf/book/9781513563602/ch19.pdf

- U.S. Securities and Exchange Commission. (n.d.). Individual Retirement Accounts (IRAs). Retrieved from https://www.investor.gov/additional-resources/retirement-toolkit/self-directed-plans-individual-retirement-accounts-iras

- U.S. Securities and Exchange Commission. (n.d.). Traditional and Roth 401(k) Plans. Retrieved from https://www.investor.gov/additional-resources/retirement-toolkit/employer-sponsored-plans/traditional-and-roth-401k-plans

Calling this number connects you to one of our trusted partners.

If you're interested in help navigating your options, a representative will provide you with a free, no-obligation consultation.

Our partners are committed to excellent customer service. They can match you with a qualified professional for your unique objectives.

We/Our Partners do not offer every plan available in your area. Any information provided is limited to those plans offered in your area. Please contact Medicare.gov or 1-800-MEDICARE to get information on all of your options.

866-923-9782Your web browser is no longer supported by Microsoft. Update your browser for more security, speed and compatibility.

If you need help pricing and building your medicare plan, call us at 844-572-0696