Qualified vs. Non-Qualified Annuities

Qualified and non-qualified are terms that characterize how the IRS treats annuities and other retirement-focused financial products at tax time. Both qualified and non-qualified annuities offer powerful savings advantages, but qualified annuities are typically tax-deductible while non-qualified annuities are not.

- Written by Dori Zinn

- Edited By

Lamia Chowdhury

Lamia Chowdhury

Financial Editor

Lamia Chowdhury is a financial content editor for RetireGuide and has over three years of marketing experience in the finance industry. She has written copy for both digital and print pieces ranging from blogs, radio scripts and search ads to billboards, brochures, mailers and more.

Read More- Reviewed By

Ebony J. Howard, CPA

Ebony J. Howard, CPA

Credentialed Tax Expert at Intuit

Ebony J. Howard is a certified public accountant and freelance consultant with a background in accounting, personal finance, and income tax planning and preparation. She specializes in analyzing financial information in the health care, banking and real estate sectors.

Read More- Published: November 29, 2021

- Updated: May 21, 2025

- 5 min read time

- This page features 4 Cited Research Articles

- Reviewed By

One of the key features of annuities is their ability to grow tax-deferred, which means investment earnings are not taxed until they are paid out to the purchaser. However, there are IRS rules that govern if and when annuity taxes are due on the premium, which is the money you used to purchase the annuity.

These rules are characterized by the terms qualified and non-qualified. Qualified and non-qualified annuities differ in a number of ways — most importantly in how they are purchased and taxed.

*Ad: Clicking will take you to our partner Annuity.org.

How Are Qualified and Non-Qualified Annuities Different?

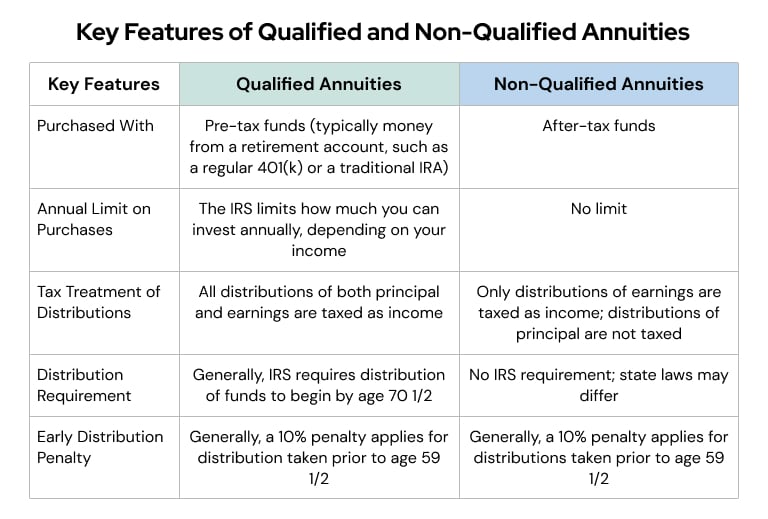

A qualified annuity allows for a tax-deductible purchase (made with pre-tax dollars), while a non-qualified annuity involves a purchase made with money which has already been taxed. Moreover, when you receive a distribution from a qualified annuity, the entire amount — premium and earnings — is subject to ordinary income tax.

With a non-qualified annuity, only the earnings component is taxable since you already paid tax on the money used to make the purchase.

Another important distinction is the money used to buy the annuity. A qualified annuity can only be purchased with money from another type of qualified vehicle, such as a regular 401(k) plan or a traditional individual retirement account (IRA). An annuity purchased with a non-qualified source of money is automatically classified as non-qualified.

The Basics of Qualified Annuities

A qualified annuity is a tax-advantaged financial product that can help you save for retirement. This is because the premium is allowed to grow tax-deferred, which can have a powerful cumulative effect over time.

You won’t pay taxes on the premium or the accumulated earnings until your annuity begins paying out, which usually occurs in retirement. However, the money used to buy a qualified annuity must come from another source of IRS-qualified funds.

- Regular 401(k) plans

- Regular 403(b) plans

- Traditional IRAs

- Simplified Employee Pension (SEP) plans

- Tax-exempt savings plans

In addition to the funding source restriction, the IRS limits how much you can contribute to a qualified annuity annually. The limit depends on your income and the extent to which you participate in other qualified savings plans.

If you make withdrawals before turning 59 and a half, you could face a 10 percent tax penalty. All distributions are subject to ordinary income tax, regardless of what age you take them.

In some instances, the money in a qualified annuity can be transferred into a similar qualified annuity without triggering a tax liability. This transaction is known as an IRS 1035 exchange.

- Earn a higher rate of return

- Reduce fees

- Take advantage of enhanced features offered by another annuity

- Move the money to a more financially sound insurance company

*Ad: Clicking will take you to our partner Annuity.org.

The Basics of Non-Qualified Annuities

While a qualified annuity is purchased with pre-tax money and subject to contribution limits, a non-qualified annuity is purchased with after-tax dollars and has no contribution limits.

As a result, the purchase of a non-qualified annuity is not connected to IRS-qualified plans, such as 401(k) plans and traditional IRAs. The money used to purchase a non-qualified annuity can come from anywhere, like savings accounts, taxable brokerage accounts, and inheritances.

Since the money used to purchase a non-qualified annuity has already been taxed, it will never be taxed again. But you will get taxed when you begin taking distributions — unless the annuity was purchased within a Roth 401(k) plan or a Roth IRA. Earnings in Roth-style accounts are not taxable.

As with qualified annuities, non-qualified withdrawals before you turn 59 and a half years of age are subject to a 10 percent IRS penalty and a non-qualified annuity can be transferred via a 1035 exchange in certain circumstances.

Retirement Considerations

Annuities are often purchased and customized to meet retirement objectives. For many retirees, these products provide a great way to achieve a guaranteed stream of income in a low-risk, hands-off manner.

Both qualified and non-qualified annuities can help you save for retirement. But there are a number of differences between them, including tax deductibility, annual purchase limits, and distribution requirements.

Carefully consider all of these before you purchase an annuity. If you end up buying one, you’ll need to arrange how to eventually receive your distributions.

- A lump-sum payment

- A stream of fixed payments for a set period of time

- A stream of fixed payments for life

Depending on your unique circumstances, any of one of these options could be optimal. Be aware that the lump-sum payment option could result in a sudden and significant tax liability, while the payment stream alternatives will spread your tax liability over time.

Regardless of your situation, remember that annuities are just one way to plan for retirement. Consider talking to a financial advisor about all of the ways you can save and invest and whether an annuity is sensible for your financial circumstances.

Frequently Asked Questions About Qualified and Non-Qualified Annuities

Connect With a Financial Advisor Instantly

Our free tool can help you find an advisor who serves your needs. Get matched with a financial advisor who fits your unique criteria. Once you’ve been matched, consult for free with no obligation.

- Published in top outlets, such as the New York Times, Wall Street Journal, CNN and more

- President of Blossomers Media, Inc.

- Bachelor’s degree in Multimedia Journalism from Florida Atlantic University in Boca Raton, Florida

4 Cited Research Articles

- IRS.gov. (2025, February 18). Traditional IRAs. Retrieved https://www.irs.gov/retirement-plans/traditional-iras

- IRS.gov. (2025, January 30). 401(k) Plans. Retrieved from https://www.irs.gov/retirement-plans/401k-plans

- IRS.gov. (2024, August 20). Roth IRAs. Retrieved from https://www.irs.gov/retirement-plans/roth-iras

- Investor.gov. (n.d.). Section 1035. Retrieved from https://www.investor.gov/introduction-investing/investing-basics/glossary/section-1035

Calling this number connects you to one of our trusted partners.

If you're interested in help navigating your options, a representative will provide you with a free, no-obligation consultation.

Our partners are committed to excellent customer service. They can match you with a qualified professional for your unique objectives.

We/Our Partners do not offer every plan available in your area. Any information provided is limited to those plans offered in your area. Please contact Medicare.gov or 1-800-MEDICARE to get information on all of your options.

866-923-9782Your web browser is no longer supported by Microsoft. Update your browser for more security, speed and compatibility.

If you need help pricing and building your medicare plan, call us at 844-572-0696