Return of Premium Rider for Annuities

A return of premium rider is a low-risk add-on to your annuity plan. It is a type of death benefit rider that ensures your beneficiary will receive payments if you die before the set term of the plan has elapsed. In addition, a return of premium rider may be a good replacement for a life insurance policy.

- Written by Sierra Campbell

- Edited By

Lamia Chowdhury

Lamia Chowdhury

Financial Editor

Lamia Chowdhury is a financial content editor for RetireGuide and has over three years of marketing experience in the finance industry. She has written copy for both digital and print pieces ranging from blogs, radio scripts and search ads to billboards, brochures, mailers and more.

Read More- Published: August 2, 2023

- Updated: May 21, 2025

- 8 min read time

- This page features 6 Cited Research Articles

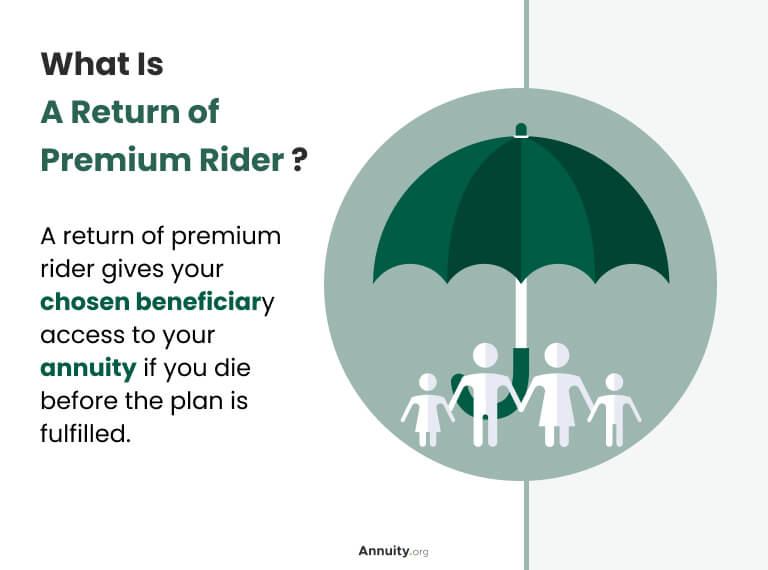

- A return of premium rider gives your chosen beneficiary access to your annuity if you die before the plan is fulfilled.

- It is a low-risk way to protect your annuity investment and provide for a beneficiary.

- This rider comes with fees but may replace the need for a life insurance policy.

What Is a Return of Premium Rider?

Most standard annuity plans will offer returns while you are alive and will terminate when you die. Like riders for your home insurance policy, a return of premium rider is an add-on to your annuity contract. This type of annuity rider ensures that the provider will return the remaining premium to your chosen recipient if you die before your annuity is fully paid out.

Why Consider a Return of Premium Rider for Your Annuity

A return of premium rider combines the stable income of an annuity with the provision for others that is common in life insurance policies – which pay out investment after your death. This type of rider offers peace of mind by ensuring any money that you don’t receive during the lifetime of your annuity is passed on to your chosen beneficiary.

Annuities offer a regular income while you are living. When you invest in an annuity, you are setting up a way to receive regular payments for the rest of your life. However, like many investments, annuities are subject to changing interest rates. An annuity calculator is a helpful tool to use when you’re considering whether an annuity plan is right for you.

The amount of money you invest in an annuity is called a premium. Your premium is paid back to you in regular increments according to the terms of your plan. After you die, your annuity contract will close, and any remaining value in the annuity returns to the provider. However, if you opt for a return of premium rider, the remaining amount in the annuity contract will be provided to your chosen beneficiary after you die.

How soon are you retiring?

What is your goal for purchasing an annuity?

Select all that apply

Learn About Top Annuity Products & Get a Free Quote

Find out how an annuity can offer you guaranteed monthly income throughout your retirement. Speak with one of our qualified financial professionals today to discover which of our industry-leading annuity products fits into your long-term financial strategy.

For fastest service, call now!

866-219-2282Call NowOr fill out the form

How Does a Return of Premium Rider Impact Your Annuity Payments?

Most return of premium riders will come with a fee, or they will increase the initial lump sum or the amount of regular payments you make into your plan. If you think you will personally benefit from your full annuity payments while you are alive, a return of premium rider may not be for you. If you think you may not receive the full benefit of your annuity plan, a return of premium rider could be beneficial for you and your beneficiary.

Potential Decrease in Payout

There are many factors that influence the payout you will receive from your annuity, including the type of annuity you choose, your life expectancy and any add-ons. For example, adding a return of premium rider to an annuity could affect the regular payouts you receive. It could also lead to additional fees and charges.

- Annuity Type

- Fixed annuities guarantee a specific payment amount. Variable annuities let you choose a specific mutual fund portfolio to invest in and the payout will depend on the performance of those funds. Indexed annuities offer a return based on the performance of a specific stock market index over a set time.

- Interest Rates

- Many annuity payouts fall when interest rates drop.

- Market Performance

- Some annuity plans include options for investment and therefore will be subject to market fluctuations.

- Age or Life Expectancy

- If you die before reaching the term of your annuity, you may not fully benefit from your investment.

- Riders and Features

- Any rider or additional features will affect the baseline terms of your annuity plan.

- Fees and Expenses

- Many annuity plans are subject to surrender charges and withdrawal fees.

Speak with an independent financial advisor about factors that could influence your annuity payouts.

Additional Cost of Rider

Annuities offer stable income during your lifetime, and riders are a good way to ensure your plan is tailored to your particular needs. But keep in mind that any annuity rider, including a return of premium rider, will affect the fees and cost implications of your plan.

- Additional Fees

- Some annuity providers may charge an annual fee or service charge for a return of premium rider.

- Impact on Potential Returns

- Riders typically cost a set percentage of the premium. This means that the annual return will drop by a percentage based on the cost. For example, say your annuity has a 6% annual rate of return and a return of premium rider costs 1% of your premium; the rider will now reduce your annual return to 5%.

- Long-Term Costs

- Any rider can reduce the total return of an annuity. When choosing a return of premium rider, the cost should be measured against the benefit of making your investment available to your beneficiary.

Is a Return of Premium Rider Right for You?

If you’re thinking about adding a return of premium rider to your annuity plan, consider any initial and ongoing costs, your personal financial goals, your time horizon and the type of investment alternatives available to you. You’ll also want to consider your investment style, financial discipline and financial flexibility. If you do not have any beneficiaries, exploring different investments or annuity riders might be a better option than a return of premium rider.

In addition, if you are in good health and have many years on your annuity plan, the additional cost of a return of premium rider may not be the right choice. However, this rider could be a good option if you do not expect to personally receive the full premium invested in your plan.

Once you have spoken with a financial advisor about which baseline annuity plan suits your needs, you can consider certain add-ons, including a return of premium rider. This may provide peace of mind in knowing that if you die before your annuity is fully paid out, any outstanding premiums will return to your beneficiary.

Assessing Your Financial Security

Annuity plans allow for stable income while you are alive. Therefore, if you are in good health, your finances are stable and you don’t have any beneficiaries to support, then a return of premium rider might not be the right choice for you. However, if you are investing in an annuity plan for a long period, a return of premium rider could ensure you and your beneficiary get the entire amount of your agreed plan, even if you do not live out the full term.

Planning for Your Family's Future

While a return of premium rider is likely to increase the cost of your annuity payments and come with fees, it may replace the need for a life insurance policy. Rather than payments ending when you die, a return of premium rider returns the total amount of your remaining annuity plan to your chosen beneficiary. The amount available to your beneficiary will depend on how much you have invested as an initial lump sum or as regular payments in your annuity.

Frequently Asked Questions About Return of Premium Riders

Editors Malori Malone and Sierra Campbell contributed to this article.

Connect With a Financial Advisor Instantly

Our free tool can help you find an advisor who serves your needs. Get matched with a financial advisor who fits your unique criteria. Once you’ve been matched, consult for free with no obligation.

6 Cited Research Articles

- Hicks, C. (2024, Dec. 18). 19 Things You Need To Know About Annuities. Retrieved from https://money.usnews.com/investing/investing-101/articles/things-you-need-to-know-now-about-annuities

- Lake, R. (2023, March 11). How Does My Annuity Rider Work? Retrieved from https://finance.yahoo.com/news/most-common-annuity-riders-175347537.html

- Investor.gov. (2023). Annuities. Retrieved from https://www.investor.gov/introduction-investing/investing-basics/investment-products/insurance-products/annuities

- Investor.gov. (2023). Variable Annuities. Retrieved from https://www.investor.gov/introduction-investing/investing-basics/investment-products/insurance-products/variable-annuities

- Investor.gov. (2020, July 31). Updated Investor Bulletin: Indexed Annuities. Retrieved from https://www.investor.gov/introduction-investing/general-resources/news-alerts/alerts-bulletins/investor-bulletins/updated-13

- Safe Annuity Education. (n.d.). Glossary. Retrieved from https://www.safeannuityeducation.org/about-annuities/common-annuity-related-terms/

Calling this number connects you to one of our trusted partners.

If you're interested in help navigating your options, a representative will provide you with a free, no-obligation consultation.

Our partners are committed to excellent customer service. They can match you with a qualified professional for your unique objectives.

We/Our Partners do not offer every plan available in your area. Any information provided is limited to those plans offered in your area. Please contact Medicare.gov or 1-800-MEDICARE to get information on all of your options.

866-923-9782